Britain's postcode penalty: Why where you buy matters more than ever

Cesca Newton

Cesca NewtonTembo's latest First-Time Buyer Index reveals Britain's housing divide is widening. We're calling it the postcode penalty: where exactly the same decision to buy a first home can leave two buyers in very different financial positions simply because of where they live.

While many buyers across the North can still begin building wealth from day one, higher deposits and mortgage costs mean aspiring homeowners across much of the South face a growing financial disadvantage. The good news? Buying still wins over the long term almost everywhere... it simply takes longer in some parts of the country.

The postcode penalty is getting bigger

Andy Burnham's emergence as Labour leader has reignited debate over how Britain taxes property, with proposals to replace council tax and stamp duty with a land value tax returning to the political agenda. Yet Tembo's latest data suggests Britain's biggest housing divide already exists. Long before any reforms arrive, where you live increasingly determines whether buying your first home makes financial sense.

Our latest First-Time Buyer Index shows the gap between northern and southern buyers widened again during Q2 2026. Rising mortgage rates and climbing house prices made affordability more challenging across the UK, but the impact has been anything but equal.

Across much of the North, relatively affordable house prices still allow buyers to begin building wealth immediately. In many southern cities, however, larger deposits and significantly higher monthly repayments mean the financial rewards of buying take much longer to emerge.

National housing headlines matter less than they once did. Increasingly, local affordability, borrowing power and house prices are shaping buyers' financial outcomes far more than the national picture.

Quite simply, your postcode is becoming one of the biggest predictors of whether buying today makes financial sense.

See what you could afford today with Tembo

Get certainty on your best mortgage options from +100 lenders online today with Tembo, the UK's Best Mortgage Broker for four years running.

Affordability has worsened...

After almost two years of improving affordability, progress stalled this quarter.

House prices rose across 14 of the 21 cities analysed, while deposits increased in 70% of locations and mortgage repayments climbed as interest rates rose through April and May.

Those combined pressures pushed Tembo's First-Time Buyer Attractiveness Score down to 589, moving it from the High category into Moderate. In practical terms, that means buyers are increasingly having to make trade-offs between affordability, borrowing power and location.

Ironically, affordability worsened at exactly the same time buyers gained more choice.

Our First-Time Buyer Attractiveness Score is a composite score out of 100 that reflects how “good” the market is for a first-time buyer at a given point in time, based on measures covering key themes: affordability, credit, savings and financial outcomes.

... but buyers have more choice

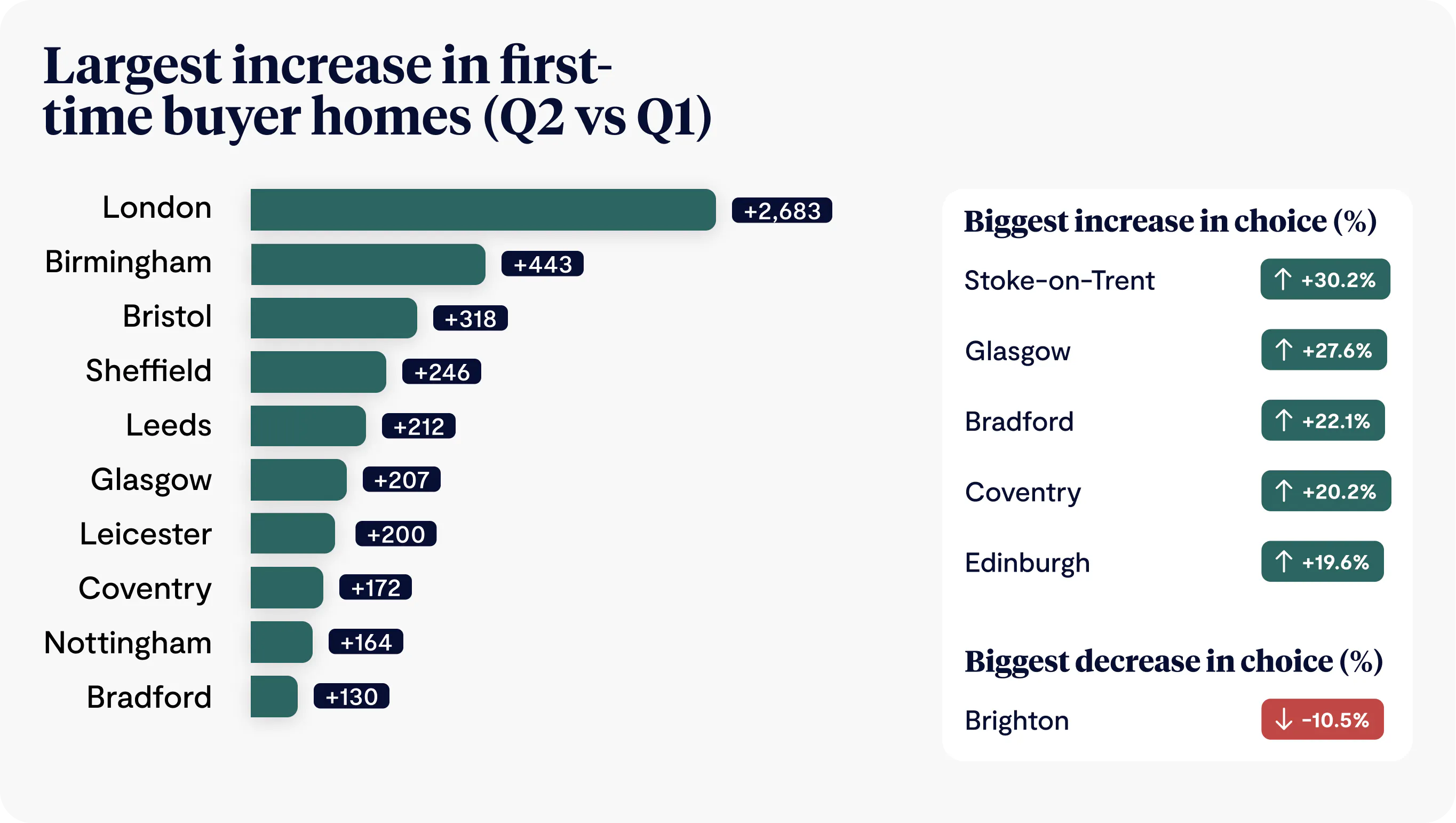

Buyers are entering a tougher market, but one with significantly more choice.

Across the UK, 21 of the 22 cities analysed recorded an increase in first-time buyer properties coming onto the market, resulting in 17% more homes being available than in Q1.

London recorded the largest increase in total listings, while Stoke-on-Trent, Glasgow and Bradford experienced the strongest percentage growth.

Brighton was the only city where first-time buyer stock declined.

More homes won't solve affordability on their own, but increased choice gives buyers greater opportunity to find properties that better fit their budgets, negotiate more effectively and act when the right opportunity appears.

The postcode penalty in numbers

National averages only tell half the story. Once the data is split by region, the scale of Britain's postcode penalty becomes impossible to ignore.

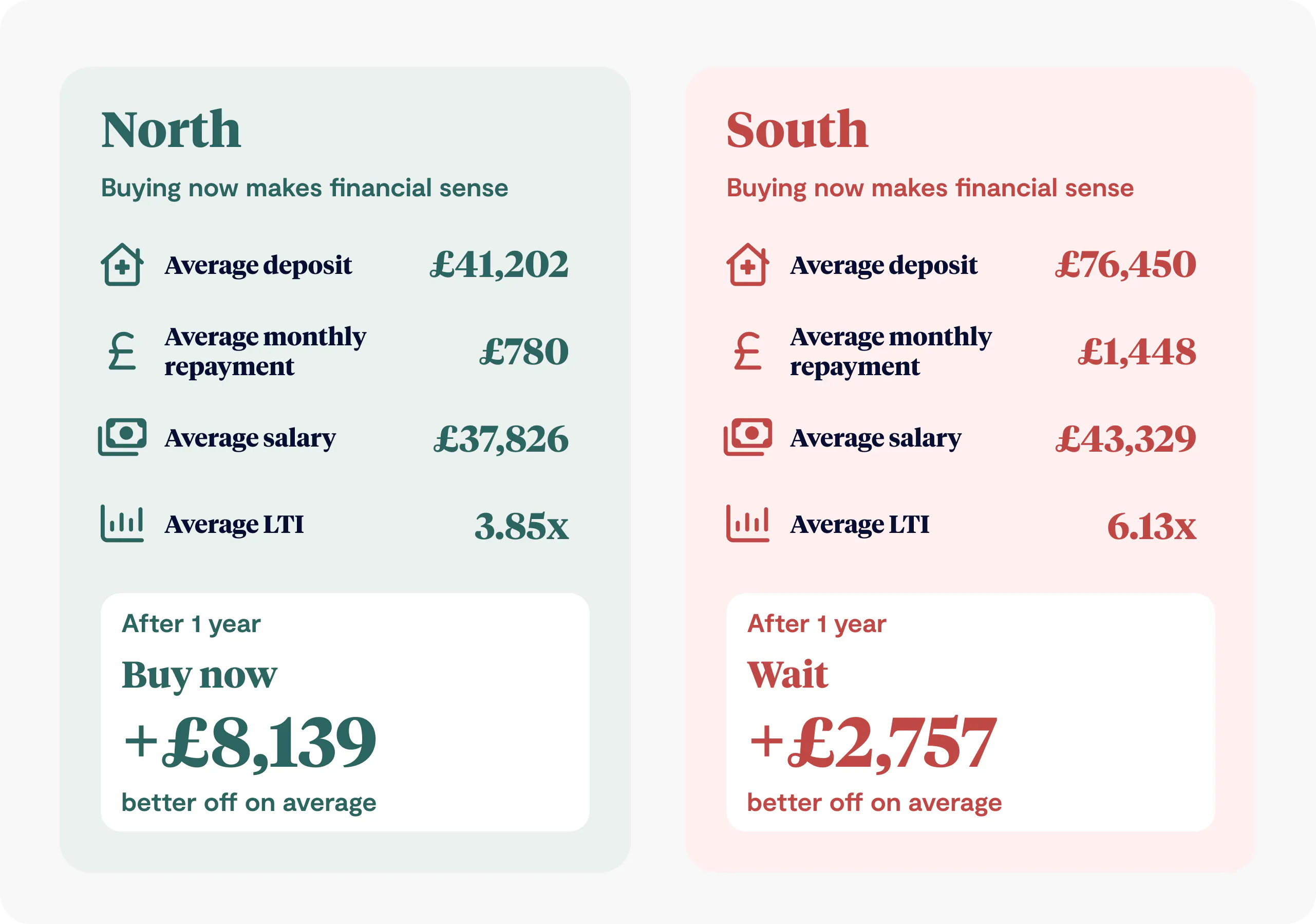

Across northern cities, the average first-time buyer needs a deposit of £41,202, pays around £780 per month on their mortgage and typically borrows at 3.85 times their income.

Across southern cities, those figures jump dramatically. Buyers now need an average deposit of £76,450, face average monthly repayments of £1,448, and require borrowing of 6.13 times their income. Although salaries are around 15% higher, that increase comes nowhere near offsetting today's borrowing costs.

Buying still wins (it just takes longer)

One of the biggest misconceptions in today's market is that higher borrowing costs mean homeownership no longer builds wealth. Our data suggests the opposite.

In the short term, waiting can sometimes make financial sense in higher-cost markets. Across the North, buying immediately leaves the average first-time buyer £8,139 better off after one year. Across the South, waiting another year currently leaves would-be buyers £2,757 better off on average.

However, the picture changes dramatically over time.

Over a five-year horizon, homeownership remains one of the most effective long-term wealth-building tools available. Compared with continuing to rent and investing a deposit, buying generates an average of:

- £48,851 more wealth across the North

- £19,558 more wealth across the South

The conclusion isn't that buying doesn't work in southern England. It's that the financial payoff arrives later. Higher upfront costs delay the benefits, but they don't remove them.

The best places to buy in Britain

While national affordability has weakened, several cities continue to stand out.

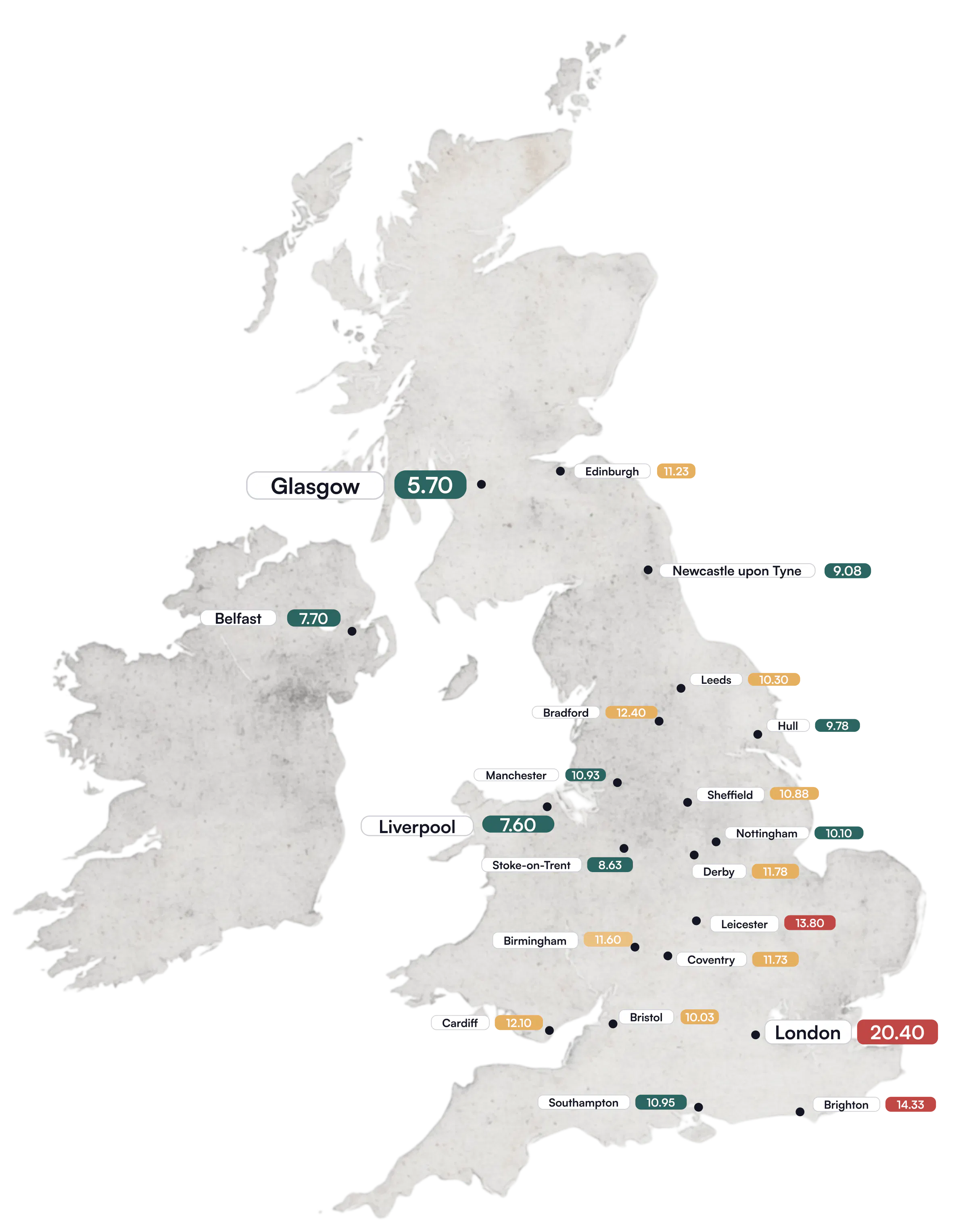

Glasgow once again tops the rankings thanks to its combination of affordability, borrowing power and long-term returns. Liverpool and Belfast remain close behind, continuing to demonstrate why they are among the UK's strongest markets for first-time buyers.

This quarter's biggest success story, however, is Hull, which climbed seven places after combining exceptional affordability with strong borrowing power and long-term financial returns. Sheffield and Leeds also posted impressive gains.

At the other end of the table, Manchester and Coventry recorded the largest falls, driven primarily by worsening affordability rather than weaker housing markets.

London remains firmly rooted at the bottom of the rankings.

Despite offering the UK's highest salaries, buyers still require an eye-watering 8.66x income multiple to purchase the average first home - perhaps the clearest illustration yet that earning more doesn't necessarily make buying easier.

What this means for first-time buyers

This quarter's data tells a more nuanced story than simply asking whether now is a good time to buy.

For buyers across many northern cities, today's market continues to offer compelling long-term value. Lower entry costs mean homeowners begin building equity immediately while also benefiting from house price growth.

In higher-cost markets, particularly across southern England, buyers may need to take a longer-term view. While waiting can sometimes make financial sense over the next twelve months, homeownership continues to deliver substantial wealth creation over five years.

Rather than asking one national question "Is now a good time to buy?", buyers increasingly need to ask a local one:

"What does buying look like where I live?"

Because in 2026, the biggest factor shaping your first home isn't just mortgage rates. It's your postcode.

Beating the postcode penalty

Whether you're buying in Manchester, Bristol, London or Glasgow, understanding your local market, exploring lenders beyond the high street and getting expert advice can make a significant difference to both what you can borrow and how quickly buying starts to pay off. At Tembo, we search over 100 lenders and more than 25,000 mortgage products to help first-time buyers find the right route onto the property ladder, wherever they live.

Tembo First Time Buyer Index - Top 20 UK Cities

| Rank Q2 2026 | City | Overall score (/21) | Position Q1 2026 |

|---|---|---|---|

1 | Glasgow | 5.70 | 1 |

2 | Liverpool | 7.60 | 2 |

3 | Belfast | 7.70 | 3 |

4 | Stoke-on-Trent | 8.63 | 8 |

5 | Newcastle upon Tyne | 9.08 | 4 |

6 | Hull | 9.78 | 13 |

7 | Bristol | 10.03 | 7 |

8 | Nottingham | 10.10 | 5 |

9 | Leeds | 10.30 | 14 |

10 | Sheffield | 10.88 | 16 |

11 | Manchester | 10.93 | 6 |

12 | Southhampton | 10.95 | 9 |

13 | Edinburgh | 11.23 | 11 |

14 | Birmingham | 11.60 | 15 |

15 | Coventry | 11.73 | 10 |

16 | Derby | 11.78 | 12 |

17 | Cardiff | 11.73 | 17 |

18 | Bradford | 12.40 | 18 |

19 | Leicester | 13.80 | 19 |

20 | Brighton | 14.33 | 20 |

21 | London | 20.40 | 21 |

About the Tembo First Time Buyer Index

The Tembo First Time Buyer Index tracks affordability across the housing market for first-time home buyers, using sold prices, mortgage valuations and data for recently agreed sales. The methodology

The Tembo data used in this report is derived from mortgage details submitted by 8,000 prospective and actual first-time buyers, 1,000 Lifetime ISA savers and credit data from 100 first-time buyers.

Calculation of First-Time Buyer Attractiveness Score

The First-Time Buyer Attractiveness Score is a weighted composite score out of 1000, combining metrics such as loan-to-income ratios, interest rates, average disposable

income after mortgage repayments, loan-to-value ratios, time to sell properties, credit profiles, and five-year buy vs rent outcomes. Metrics are grouped into five categories -

affordability, deposit, time to buy, credit and financial outcomes - and aggregated

using predefined weightings.