The UK's Best Mortgage Broker

As voted by our customers, five years running

The home for first-time buyers

Buying your first home can feel overwhelming. That's where our award-winning savings and mortgage platform comes in. By your side from your first £1 saved until you get your keys, with expertise at every step from the UK's Best Mortgage Broker five years in a row.

As seen in

By your side from the first £1 saved to buying your dream home

Get a tailored homebuying plan

How to get started:

Best fixed rate mortgages

Your interest rate stays the same for a set period, giving you certainty and stability.

Best variable rate mortgages

Your rate moves with the market, offering flexibility.

How do mortgage deals work?

Our essential guide walks you through how mortgage rates work, in everyday language.

Discover your true buying budget from +100 lenders

Discover your true buying budget from +100 lenders

Best fixed rate mortgages

Your interest rate stays the same for a set period, giving you certainty and stability.

Best variable rate mortgages

Your rate moves with the market, offering flexibility.

How do mortgage deals work?

Our essential guide walks you through how mortgage rates work, in everyday language.

Specialist mortgages

Why use Tembo?

Our service is designed to guide you through the whole process of buying your first home, with award-winning mortgage advice from start to finish.

Save your deposit

Save faster with our market-leading Lifetime ISA. Open or transfer today.

House hunt

Get a Mortgage in Principle online for free in minutes, ready to start house viewings

Put in an offer

Get free property reports to help you offer on your dream home with confidence

Find your best mortgage deal

Through our award-winning mortgage service, voted the UK's Best Mortgage Broker five years running.

Your own dedicated team

By your side from the first hello to getting your keys to your new home.

Access to our panel of conveyancers

Tried & tested paid legal guidance from our panel of experts

Trusted by thousands of first time buyers across the UK

Our mission is to make home happen for the next generation of first home buyers. We simplify the process, cut through the jargon, and use our expertise and award-winning smart tech to find all the ways you could buy sooner, including how you could boost your budget.

Single income first-time buyer

Buying with complex income

First-time buyer in London

Using income to boost affordability

Remortgaging to gift a deposit

Acting as a silent guarantor

Your first-time buyer toolkit

Tools and calculators

Stamp duty calculator

Work out what you may have to pay in Stamp Duty on your first home.

Got questions? We've got answers

See all FAQsFrequently asked questions

Save for

4.30% AER

or

Stocks & Shares

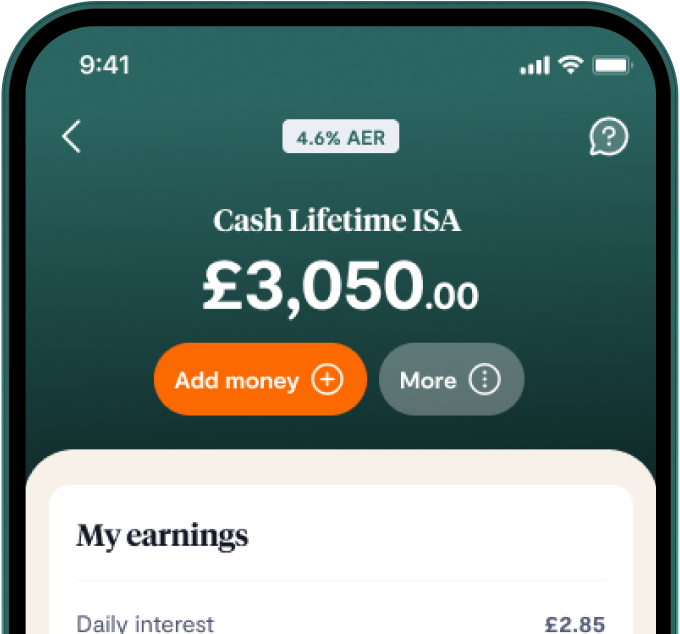

Lifetime ISA

Save up to £4,000 per tax year

25% Gov bonus of up to £1,000

Cash (4.30% AER variable) or Stocks & shares

4.05% AER

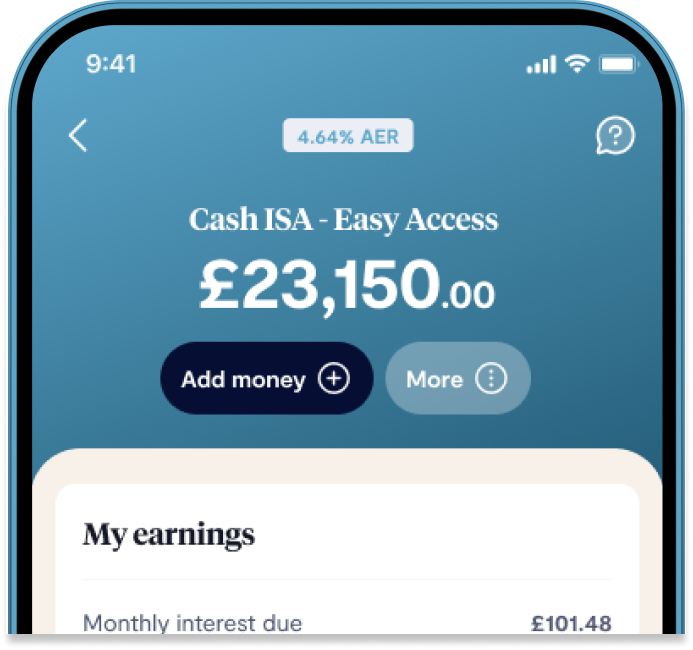

Cash ISA - Easy access

Unlimited instant withdrawals

Earn up to 3x interest vs Big 4 Banks

Up to 4.05% AER (variable)

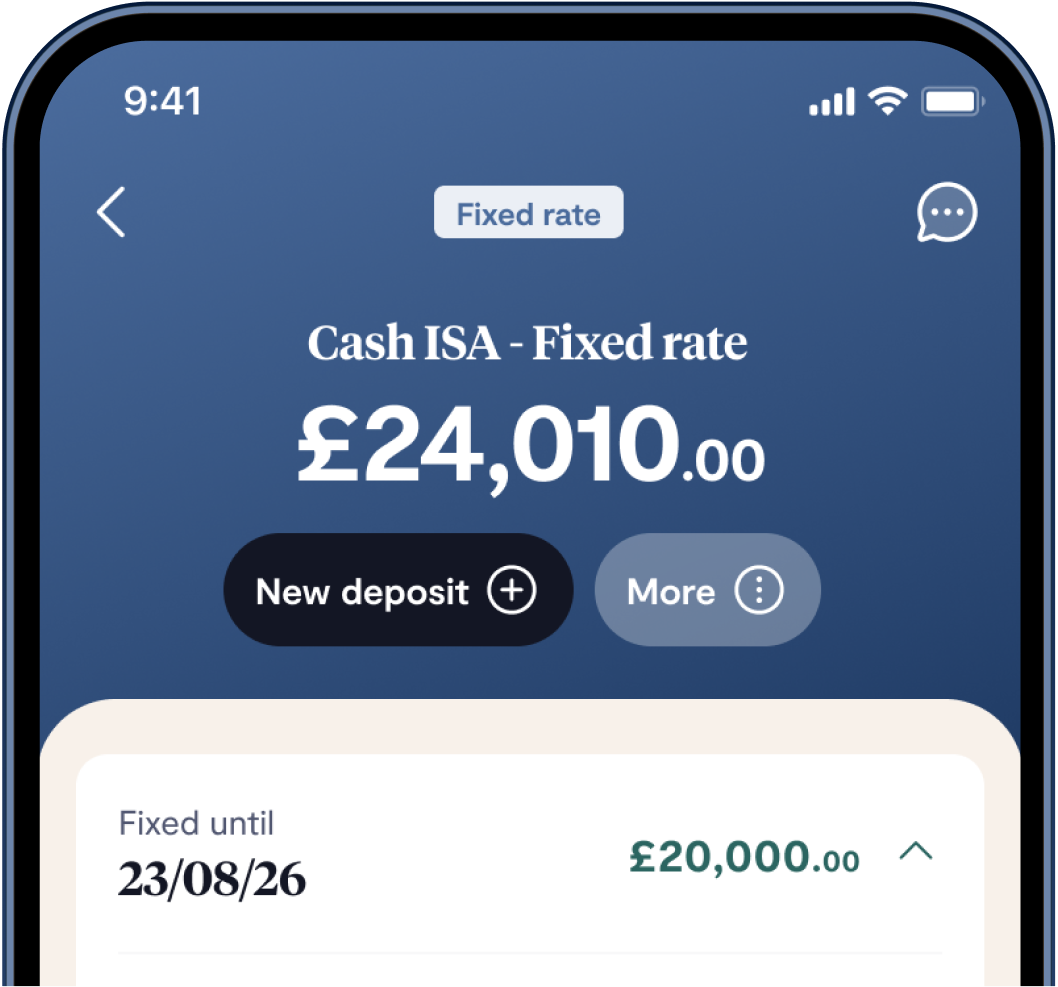

4.60% AER Fixed

Cash ISA - Fixed rate

Fixed interest rate for 12 months

Provided by Investec

Add up to £20,000 each tax year

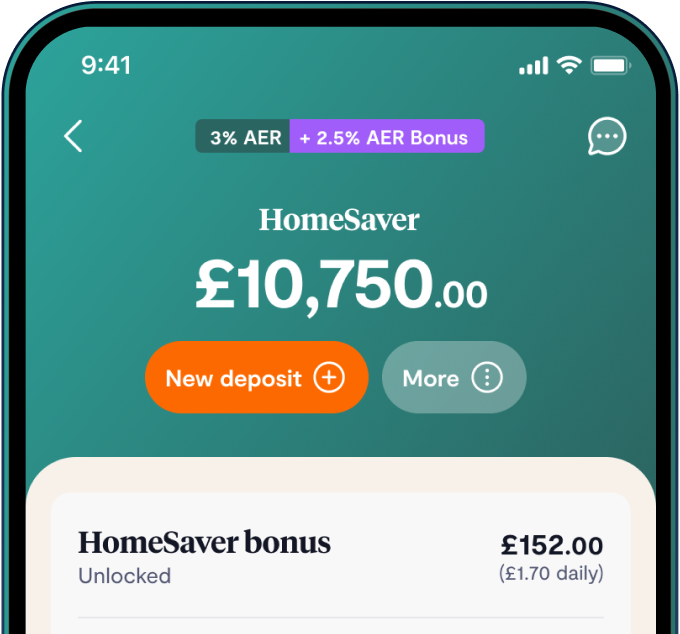

5.55% AER

HomeSaver®

4.55% AER (variable) + 1.0% 12 month bonus

Bonus unlocked when you take out a mortgage through Tembo

FSCS protection & No withdrawal limits

*Fee-free mortgage advice is subject to eligibility, see terms & conditions here. Best Mortgage Deal Guarantee subject to eligibility, see terms & conditions here