Is now a good time to buy a house?

Deciding whether to buy a house is one of the biggest financial choices you'll make. It’s not just about finding the right property; it’s about timing, affordability, and your personal circumstances.

In this guide, we walk through what’s predicted for the UK housing market in 2026 and key factors to help you decide if next year is the right time for you to step onto or move up the property ladder.

Buying a home? Earn 5.55% AER (variable) on your savings while you save

Mortgages can feel like a maze of paperwork and decisions. With HomeSaver, there'll be a reward waiting for you at the finish line, whether you're buying your first place, your next, or remortgaging.

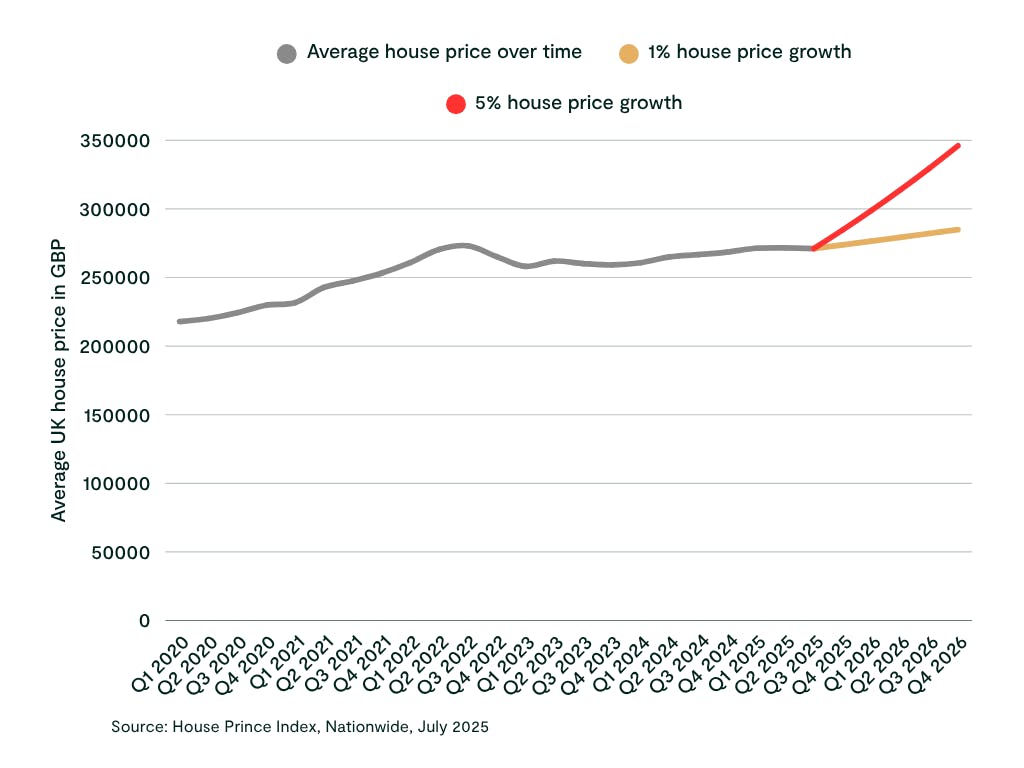

What will happen to house prices in 2026?

Most property pros are betting on the housing market cooling off a bit in 2026. No cliff-edge price drops - just a gentle, steady rise in house prices, likely between 1% and 5%. It’s a far cry from those whirlwind years of rapid growth. But this could give buyers a little more time and space to weigh up their options.

Here’s why this could work in your favour:

- More homes on the market: With more sellers (think landlords or folks with second homes) possibly deciding to sell, you could see more choice out there. With more supply, it could maybe even a bit of wiggle room on price. Read our tips on how to negotiate on house price.

- Regional differences: Not every area plays by the same rules. If you’re hunting for value, the North West, Midlands, or parts of Scotland are places to watch. Busy cities like Manchester and Liverpool are still in demand. If you’ve got your sights set on London or the South East, expect higher prices.

- The economic backdrop: If inflation stays in check and wages creep up, buyers tend to feel more confident - which could help steady the market and keep those wild price swings at bay.

What will mortgage rates do in 2026?

Mortgage rates are expected to continue easing during the remainder of 2026, although any reductions are likely to be gradual rather than dramatic. Much will depend on future decisions from the Bank of England and whether inflation continues to move towards its 2% target.

The Bank of England has kept the Bank Rate at 3.75%, and while markets expect further cuts over time, policymakers have indicated they’ll continue to take a cautious, data-driven approach. If inflation continues to ease, mortgage rates could edge lower over the coming months, but borrowers shouldn’t expect a sharp fall in rates.

If mortgage rates continue to ease, here’s what you could expect:

- Lower monthly payments: Falling mortgage rates can reduce your monthly repayments and may improve how much you can borrow, depending on your circumstances.

- More competitive mortgage deals: As funding costs fall and expectations for future interest rates improve, lenders may introduce more competitive fixed-rate mortgage products or reduce rates on existing deals.

- Lock in a rate with confidence: Many lenders allow you to secure a mortgage offer for up to six months. If rates fall further before you complete, your broker may be able to help you switch to a better deal. If rates rise instead, you’ll already have a rate locked in.

Top Tip

Many lenders factor future rate cuts into their mortgage products when they ‘price’ (set an interest rate on a fixed-term mortgage), so changes to the base rate won’t necessarily result in mortgage interest rates decreasing too.

See what rate you could be offered without applying

When you complete your mortgage options with Tembo, our smart tech will compare your eligibility to thousands of mortgage products to find all the ways you could buy sooner or remortgage.

When is the best time to buy a house?

Historically, spring and autumn are the busiest periods in the year for buying a house, as there are more houses available, and people are eager to get the ball rolling if they've decided this is the year to get on the ladder. Summer and winter tend to be quieter, so these can be good times to buy a house when there is a dip in house-hunting. When there is less demand, you could find you're able to bag a bargain.

However, during uncertain economic times, buying a house can feel riskier, regardless of the time of year. High inflation and higher mortgage interest rates may make you think that right now is a bad time to buy a house. However, if you can afford to get a mortgage now, don't let scary headlines put you off.

Is 2026 the right year for you to buy?

While the market is important, the biggest factor when deciding whether to buy a home in 2026 is you. Are your finances ship-shape? Does buying right now line up with your plans? Before you spend hours scrolling Rightmove “just in case,” get your basics covered:

- Grow your deposit: Aim for a down payment of at least 10-20%. The bigger your deposit, the better your chance of nabbing a great mortgage rate.

- Spruce up your credit score: This matters more than you think! Pay off old debts, shut down cards you don’t use, and keep up with all your payments (plus, make sure you’re on the electoral roll).

- Plan for the full cost of owning: Your monthly loan isn’t the only outlay - remember stamp duty, legal fees, as well as ongoing costs like council tax, insurance, and the odd surprise plumber bill.

Should I buy a house now or wait until 2027?

Ultimately, the decision to buy a house now or wait until 2027 hinges on your personal financial situation and readiness. While market conditions fluctuate, the most significant factor is your ability to comfortably afford a mortgage and all associated homeownership costs.

If your finances are in order – with a solid deposit, good credit score, and a clear understanding of ongoing expenses – then buying sooner might be a viable option. If you need more time to save, improve your credit, or plan for future costs, waiting could be the smarter move.

If you think you can't buy right now, you might be surprised! At Tembo, we specialise in helping buyers discover their true buying budget. In fact, on average we boost our customers' budgets by £82,000! It's easy to discover all the ways you could get on the ladder, just create a free Tembo plan in minutes!

Discover all the ways you could boost your budget

When you complete your mortgage options with Tembo, you'll get a personalised recommendation on what specialist buying schemes you're eligible for. Find out how much you could boost your buying budget through one of these schemes by creating a free plan today.