Tembo Market Watch: May 2026

Anya Gair

Anya GairThe UK housing market is sending mixed signals right now. Average house prices were unchanged in March at £268,000, mortgage rates are pulling in different directions depending on which lender you ask, and inflation, while falling, is still keeping the Bank of England cautious. If you're trying to work out whether to buy, move, or remortgage right now, here's what you actually need to know - from the UK's Best Mortgage Broker for five years running.

Key takeaways

- Mortgage rates remain unpredictable, with some lenders cutting deals while others increase rates. Now, the lowest rate available across Tembo's panel of over 100 lenders is 3.96%*.

- Inflation has eased to 2.8%, but future rises could push mortgage rates higher again.

- House prices have stalled, giving buyers more negotiating power and stability, although there are differences by region.

- Holding out for mortgage rate drops could cost you. Remortgagers should act early to avoid rolling onto costly standard variable rates; see what rate you could get today from +100 lenders

- Although the average savings rate is currently at 3.55% - higher than inflation - many savers could be on a lower rate, meaning the purchasing power of their money is actually reducing over time. Savers should review their accounts regularly to ensure their money is beating inflation, and consider switching if they aren’t.

Let’s break down exactly what’s happening and what this means for you.

Should you lock in a rate now or wait?

Navigating mortgage deals can be tricky, especially with rates changing and new products popping up all the time. Our team of award-winning mortgage experts can help you find the right mortgage deal for you, and with our free RateCheck service, your dedicated advisor can reapply for you down the line if rates drop**

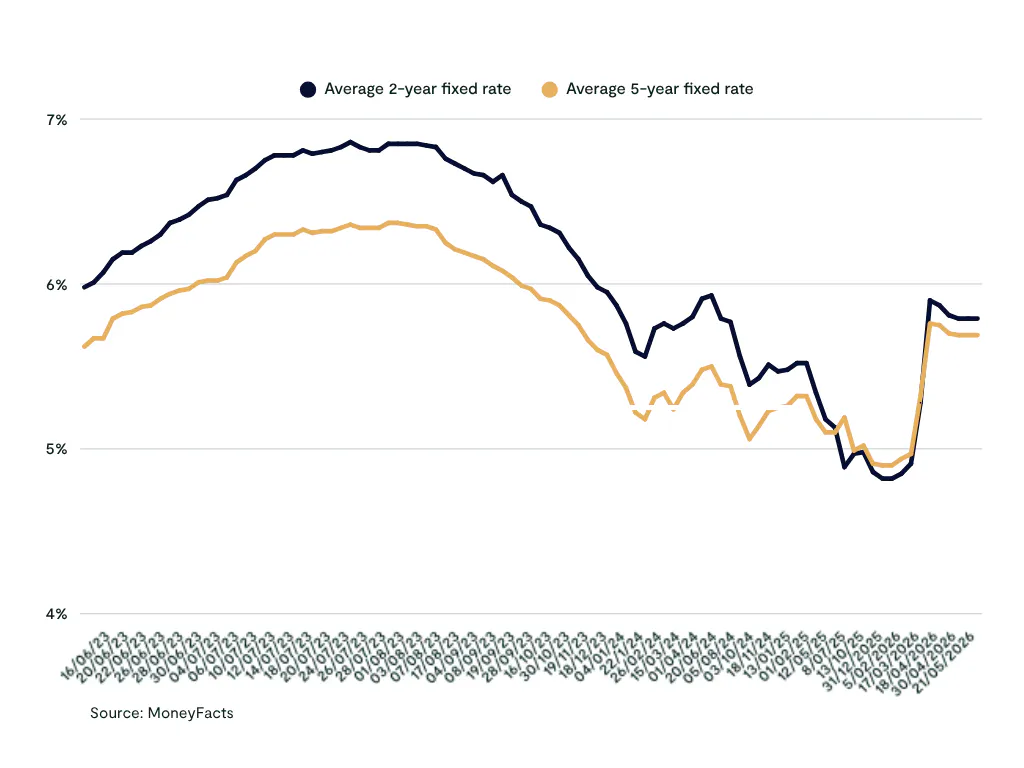

What's happening to UK mortgage rates right now?

Mortgage lenders are moving in opposite directions right now, with a lot of volatility in the market. Santander has recently cut its first-time buyer mortgage rates by up to 0.23% for buyers with 5-15% deposits (85% - 95% LTV). Other big names like Barclays have also cut some of their high-LTV products. NatWest, however, has moved the other way, raising selected rates by up to 0.2%.

Right now, the average two-year fixed rate sits at 5.78% and the five-year fix at 5.68%. But it’s important to look beyond averages, as you might be able to get a lower mortgage rate than this. Across our panel of over 100 lenders, the lowest two-year fixed rate is right now is 4.40%, while a five-year fix is 4.49%, and some tracker rates are significantly lower, with the lowest at 3.96%*. See what rate you could get today.

The latest inflation data shows that it fell more than expected from 3.3% the month before to 2.8%. However, this is expected to be short-lived, with the market anticipating inflation to rise over the summer.

If inflation does skyrocket upwards, the Bank of England may be forced to increase the base rate. Up until now, they’ve avoided doing so, and right now, the market is not expecting the base rate to be increased at their next meeting in June.

They’ll want to avoid raising the base rate until it’s absolutely necessary, as they need to balance bringing inflation back down with doing what they can to get the UK economy growing again. But if inflation does jump up, their hand may be forced. As soon as a base rate increase looks more likely, mortgage lenders may start increasing their rates in anticipation.

However, even if the base rate holds at its current level, fixed-rate mortgage deals could still climb upwards. The base rate is only one factor lenders take into consideration. Swap rates - which effectively act as a behind-the-scenes barometer for the future direction of mortgage rates - have been pushed higher more recently.

This could cause the lenders who have been cutting rates to slow down those recent improvements, or even cause mortgage rates to rise more generally.

Although some of the bigger lenders have reduced rates, others have raised theirs. There’s a lot of flip-flopping at the moment; cuts from one lender certainly aren’t a sign of a market-wide shift. It’s clear lenders are concerned with the uncertainty in the market and are more hesitant to reduce rates too quickly in case they have to put them back up the following week

Brad Wright

Senior Mortgage Advisor at Tembo

What’s happening to UK house prices?

Annual house price growth has now slowed to its lowest rate in nearly two years, down from 1.7% in the year to February. The latest data from the Office for National Statistics (ONS) showed that the average UK house price in March 2026 was £268,000, exactly the same as it was in February.

If you're thinking about moving, the regional picture matters more than the national headline. While prices in London have fallen for eight consecutive months, Wales, Scotland, and Northern Ireland are all seeing growth. Cities such as Hull, Stoke, Derby and Bradford have more affordable house prices in comparison to local incomes, which can make homeownership more accessible, while cities such as Bristol, Manchester and Edinburgh have higher loan-to-income ratios. If you're selling in a weaker market and buying in a stronger one - or vice versa - the timing of your move can also make a real difference to your position.

The good news is that mortgage approvals remain solid at a four-month high, which suggests house-buying activity is holding up despite the affordability pressures. In fact, homes are selling as fast as they were last year in more than half of the UK, despite higher mortgage rates. Considering the rocky environment over the last few months, this shows that the housing market is holding up well.

For home sellers, keep in mind that we are still in a buyer’s market. There are 5% more homes for sale than a year ago, so buyers are in a strong position to negotiate on cost. Pricing realistically is essential for a successful and quick home sale.

For first-time buyers who’ve been waiting on the sidelines, the flat house price data is, in a quiet way, useful news. House prices aren't running away from you right now, and some lenders are actively cutting rates for buyers with smaller deposits - exactly the group that often struggles most to get a foot on the ladder.

What does this mean for you?

- First-time buyers: If you are trying to get on the ladder, the current environment is still challenging for many, but certainly not hopeless. In fact, our recent report showed conditions have actually been quite favourable for first-time buyers. Get ahead of the game and explore your options now instead of waiting for a “sign”.

- Home sellers: With fewer buyers in the market, pricing realistically is crucial for a successful home sale. Keep in mind that your borrowing costs on a new property are likely to be higher than they were when you last bought. Plan around what deals currently look like, rather than chasing a moving target. See your mortgage options without applying.

- Remortgagers: This is arguably where the stakes are highest right now. If your fixed-rate deal is ending soon, the most important thing you can do is act early. Rolling onto your lender's standard variable rate - currently averaging around 7.13% - could cost you significantly more each month than locking into a new fixed or tracker deal. Get started here

See your best options from 20,000 mortgages

When you complete your details online with Tembo, our smart technology will compare your eligibility to thousands of mortgage deals across the market in minutes.

Inflation falling to 2.8% means one thing for savers

The latest data shows that inflation fell in April to 2.8%, compared to 3.3% in March. While this is good news, in some of the areas like transport and communication, which both saw prices rise by 4.5% in the 12 months to April. Plus, with so much uncertainty around events in the Middle East and energy bills set to rise again this summer, adding £209 to a typical annual bill, the next few months could still be rocky to say the least.

When your savings rate is above inflation, it means your money is maintaining its purchasing power. But although the average savings rate is currently at 3.55% - higher than inflation - many savers could be on a rate lower than inflation, meaning the purchasing power of their savings is actually degrading over time.

To avoid this happening to your hard-earned money, take a more proactive approach by reviewing your savings accounts frequently to ensure you’re earning the best rates. If your current savings rate isn’t the best on the market, and the wider perks aren’t enough to keep you there, consider switching!

If you want stability, it might be worth moving your money into a fixed rate account like a 1 Year Fixed Rate ISA, giving you certainty of earning a competitive rate for a set time period.

Remember, you can open multiple ISAs as long as you keep your deposits to your £20,000 ISA allowance for this tax year. So, you could move some of your money into a Fixed Rate ISA to benefit from the fixed interest rate, but place other funds in an easy-access Cash ISA for flexibility.

Earn a fixed 4.60% AER on your savings

Lock your savings away for 12 months with our Fixed Rate Cash ISA and earn 4.60% AER (fixed). Add more funds to lock in for 12 months from the date they're added, at the rate available at the time.

If you withdraw from the Cash ISA - Fixed Rate before maturity, you will incur a charge equal to 90 days of interest on the amount taken out. This means you may get back less than you put in. You cannot withdraw part of an immature Fixed-Rate ISA deposit; if you withdraw, you must withdraw the full balance of each deposit you select.

What should you do? Our top tips

Whether you’re thinking about buying, remortgaging or just planning ahead, here’s a clear checklist to help you make confident decisions in the current market:

- If you’re a home buyer: Understand your true budget early, and get a Mortgage in Principle so you’re ready to move when the right property appears. Get one here.

- If you’re a remortgager: If your current fixed-rate mortgage is ending within the next 6–12 months, now is the time to start exploring your options. Don’t automatically accept your lender’s standard rate; instead, see your options from across the market with Tembo.

- If you’re a saver: Periods of economic uncertainty can make budgeting feel more difficult, so make sure your money is working as hard for you as possible. Explore our range of savings accounts here.

The bottom line

The UK housing market is under real pressure from inflation and geopolitical uncertainty, but there are still meaningful opportunities for buyers, movers, and remortgagers.

Whether you are saving your first deposit, planning a move, or approaching the end of a fixed deal, the worst thing you can do right now is nothing. Understanding your options is one of the most powerful tools in your arsenal right now.

Understand how economic changes impact your mortgage options - in seconds

Complete your options online with Tembo to see your best mortgage options from across the market in minutes, all without applying. So you can make an informed decision on your next move.

Learn more

*Sourced from Tembo's lender panel, based on a 60% LTV or lower. Rates accurate 29th May 2026, subject to change. For the latest rates, please use our Mortgage Comparison tool

**Full terms and conditions of our rate checking service can be found here.