Tembo First-Time Buyer Index: January-March 2026

Anya Gair

Anya GairAt Tembo, we talk to hundreds of first-time buyers every week, all hoping to find a place they can truly call home. But for many, that sense of excitement is often tempered by uncertainty.

Today’s first-time buyers are facing one of the most challenging markets in recent history. House prices have been rising faster than wages for decades, meaning buyers now need to save much larger deposits and take on bigger loans, while also dealing with increasing rent and day-to-day living costs.

On top of that, most people haven’t been taught the fundamentals of mortgages at school, so they’re left to figure it out as they go. That often means trying to make sense of jargon, worrying headlines, and advice from friends and family that, while well-meaning, can sometimes be inconsistent.

That’s where the Tembo First-Time Buyer Index comes in. It’s designed to answer those questions and shine a light on the key trends, patterns, and changes shaping the market for first-time buyers today. Our goal is to deliver clear, data-driven insights that help buyers understand their options, identify opportunities, and feel more confident and supported on their path to owning a home.

Key takeaways:

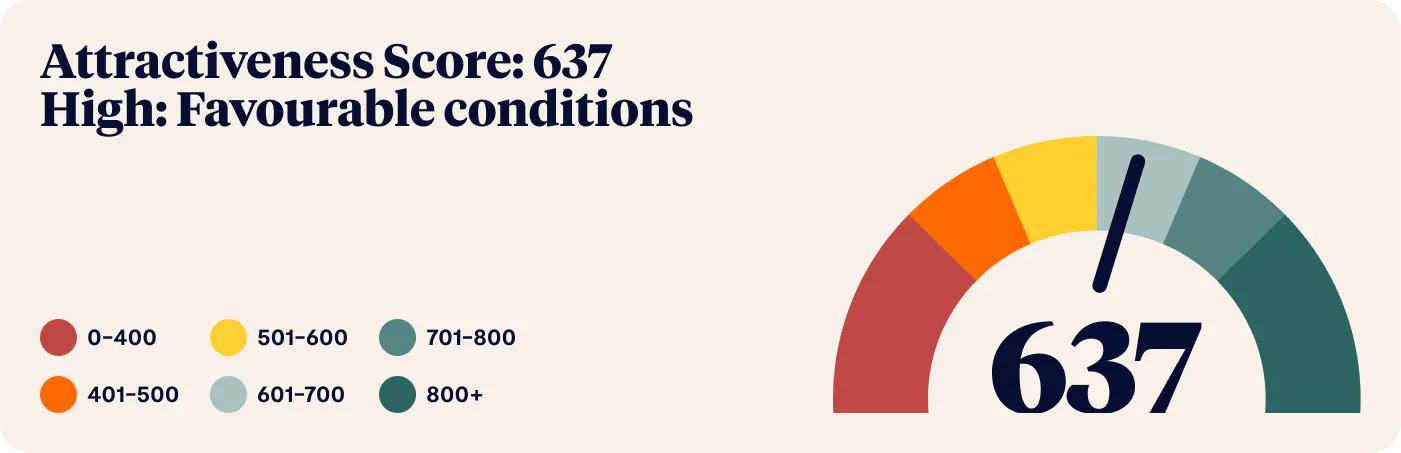

- For the first quarter of 2026, easing mortgage affordability pressures, driven by lower mortgage rates, improved access to homeownership for first-time buyers, earning a First-Time Buyer Attractiveness Score of 637.

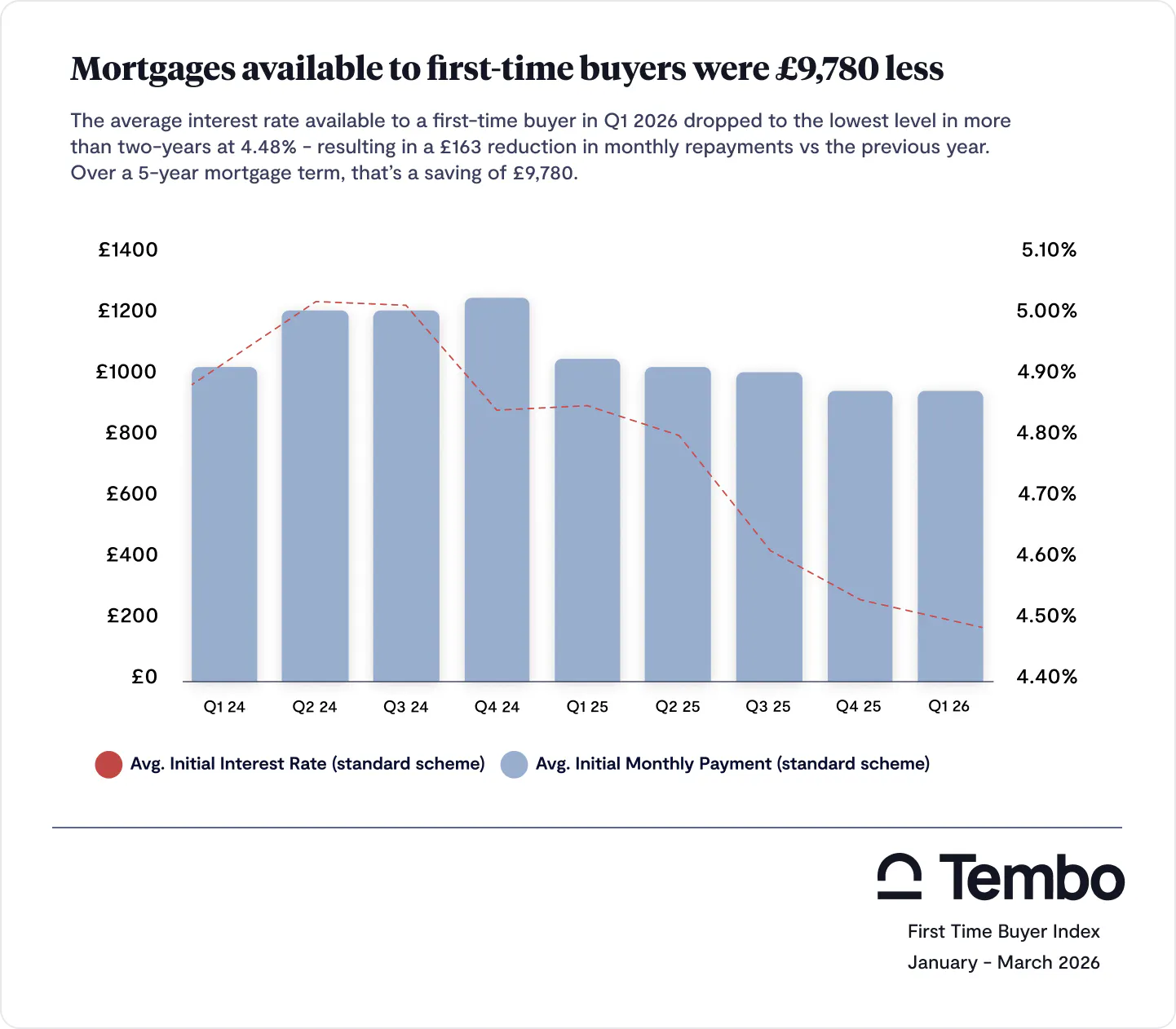

- Average interest rate available to a first-time buyer dropped to its lowest level in more than two years at 4.48%, allowing average borrowing to grow to £229,214 - an 8% reduction vs the average rate in the first quarter of 2025. Over a 5-year mortgage term, that’s a saving of £9,780.

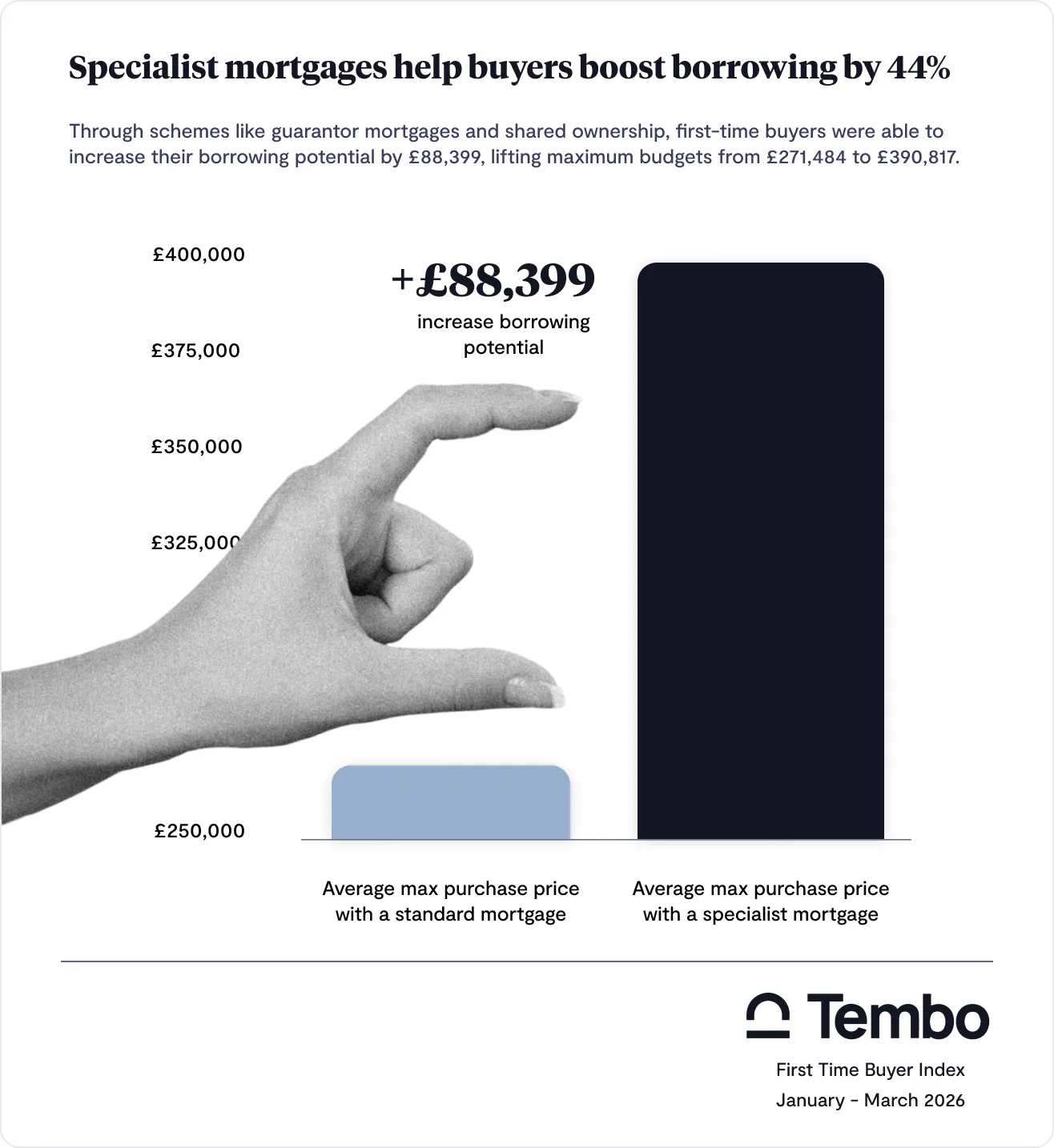

- Through specialist schemes like guarantor mortgages and shared ownership, first-time buyers were also able to increase their borrowing potential by £88,399, lifting maximum budgets from £271,484 to £390,817.

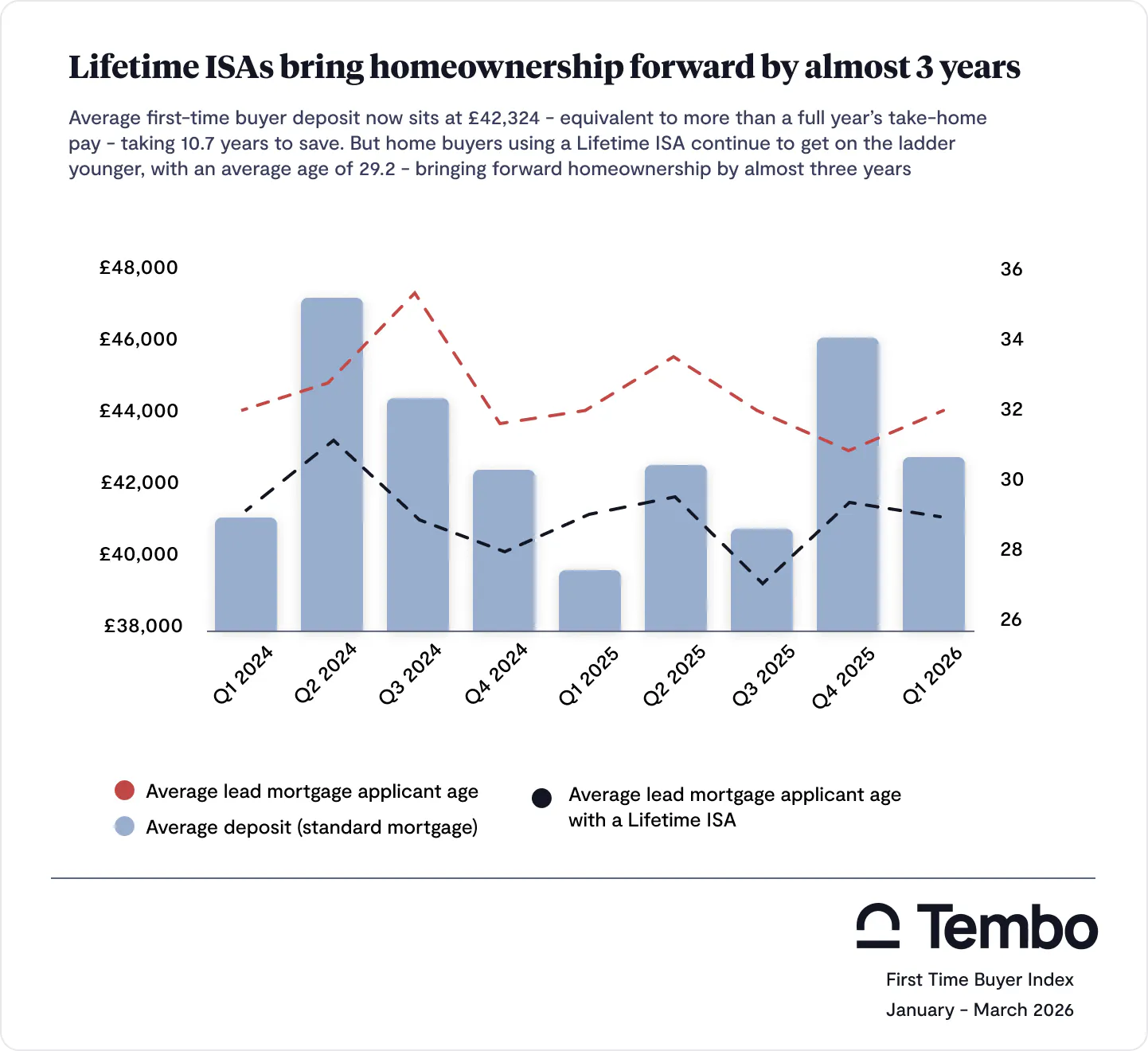

- Average first-time buyer deposit now sits at £42,324 - equivalent to more than a full year’s take-home pay. Assuming a buyer saves 10% of their income each month, that would take 10.7 years to save.

- But Lifetime ISAs can significantly speed up the time to save a deposit - cutting a year off saving for a typical first-time buyer. But only 17% of first-time buyers are using a Lifetime ISA, meaning most are missing out an estimated £3,000-£5,000 in free government support.

- Homeownership is still more profitable than renting and investing the money for a deposit instead. After 1 year, home buyers are £7,600 better off, and £64,000 better off after 5 years.

- London remains structurally unaffordable, while Glasgow comes out on top across the UK's 20 largest cities for overall attractiveness for first-time buyers. Cities like Manchester, Belfast, Bristol, Newcastle & Edinburgh all score well when assessing affordability alongside lifestyle indicators.

Is now a good time to buy a house for first-time buyers?

In the first quarter of 2026, the UK housing market had a First-Time Buyer Attractiveness Score of 637, showing that the conditions were favourable, with broad affordability for aspiring homebuyers.

Easing mortgage affordability pressures, driven by lower mortgage rates in the last few months, has supported access to homeownership. However, underlying constraints such as deposit requirements and borrowing limits remain, meaning access - while improved - is not without significant challenges.

This is not to say that getting on the ladder feels, or is, easy at an individual level, but rather reflects broader market trends.

Our First-Time Buyer Attractiveness Score is a composite score out of 100 that reflects how “good” the market is for a first-time buyer at a given point in time, based on measures covering key themes: affordability, credit, savings and financial outcomes.

See what you could afford today with Tembo

Get certainty on your best mortgage options from +100 lenders online today with Tembo, the UK's Best Mortgage Broker for four years running.

First-time buyer affordability improved in the first quarter of 2026 as average borrowing grew to £229,214

In the first quarter of 2026, first-time buyer income remained broadly flat, only 4% higher versus the last quarter of 2025, but -2% verses the same period last year, offering no tangible boost to buying power.

Despite this, the average amount borrowed by a first-time buyer grew to £229,214 after shrinking each quarter in 2025.

This increase in affordability has been driven by a significant drop in average mortgage rates. While interest rates started to climb toward the end of the quarter due to conflict in the Middle East, the average mortgage rate available to a first-time buyer fell to its lowest level in more than two years at 4.48%.

That’s an 8% reduction versus the average 4.85% seen in the first quarter of 2025. That means mortgages available to first-time buyers were £9,780 less expensive over a 5-year term vs the previous year.

This marks the third consecutive quarter of average mortgage payments making up less than 30% of net income - 30% is widely used as a “rule of thumb” for affordable housing costs, so it’s positive to see this established trend.

Specialist mortgages that boost affordability continue to play a key role in helping buyers reach even higher property prices. Through schemes like guarantor mortgages and shared ownership, first-time buyers were able to increase their borrowing potential by £88,399, lifting maximum budgets from £271,484 to £390,817.

Average deposit is equivalent to more than a full year’s take-home pay - but Lifetime ISAs help shave a year off saving

While monthly repayments have fallen, the upfront deposit remains a major barrier for first-time buyers. Our average first-time buyer deposit now sits at £42,324 - equivalent to more than a full year’s take-home pay.

Assuming a buyer saves 10% of their net income each month, it would take around 10.7 years to reach this figure! Despite this, only 17% of first-time buyers are using a Lifetime ISA to support their savings journey.

As a result, the typical first-time buyer is missing out on an estimated £3,000-£5,000 in free government support - equivalent to 7-12% of the average deposit, or cutting over a year off the time to save.

With this in mind, it's unsurprising that buyers using a Lifetime ISA continue to buy younger than the average first-time buyer, with an average age of 29.2 vs 32 - bringing forward homeownership by almost three years.

Save with the market-leading Cash Lifetime ISA

Earn 4.30% AER (variable) on your savings with the Tembo Cash Lifetime ISA. That's hundreds more in interest towards your house fund vs saving with the closest competitor over 5 years.

This reinforces the role of structured saving accounts such as the Lifetime ISA in supporting earlier entry onto the property ladder, particularly at a time when the government is consulting on the future structure of these savings scheme.

Find out more: What are Lifetime ISAs?

The maximum Lifetime ISA bonus is up to £1,000 per year. Withdrawals from a Lifetime ISA for any purpose other than buying a first home (up to a value of £450,000) or for retirement (60+) incur a 25% government penalty, meaning you may get back less than you paid in.

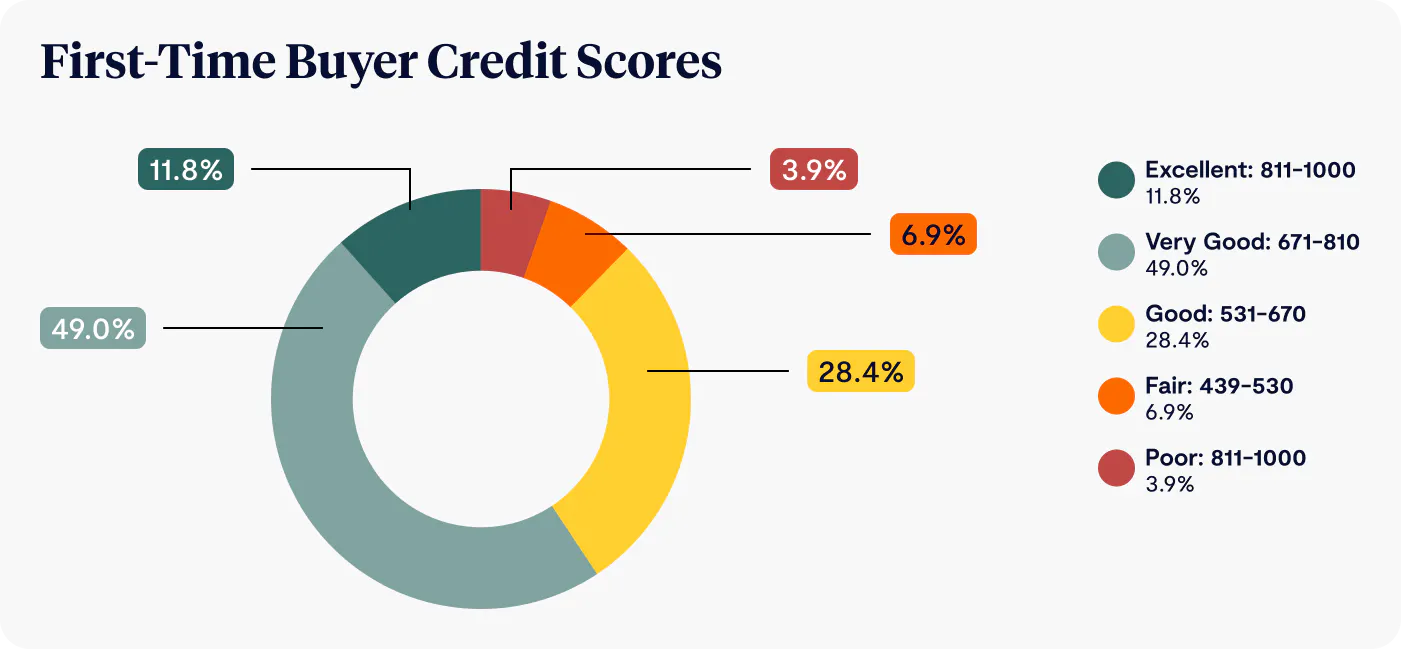

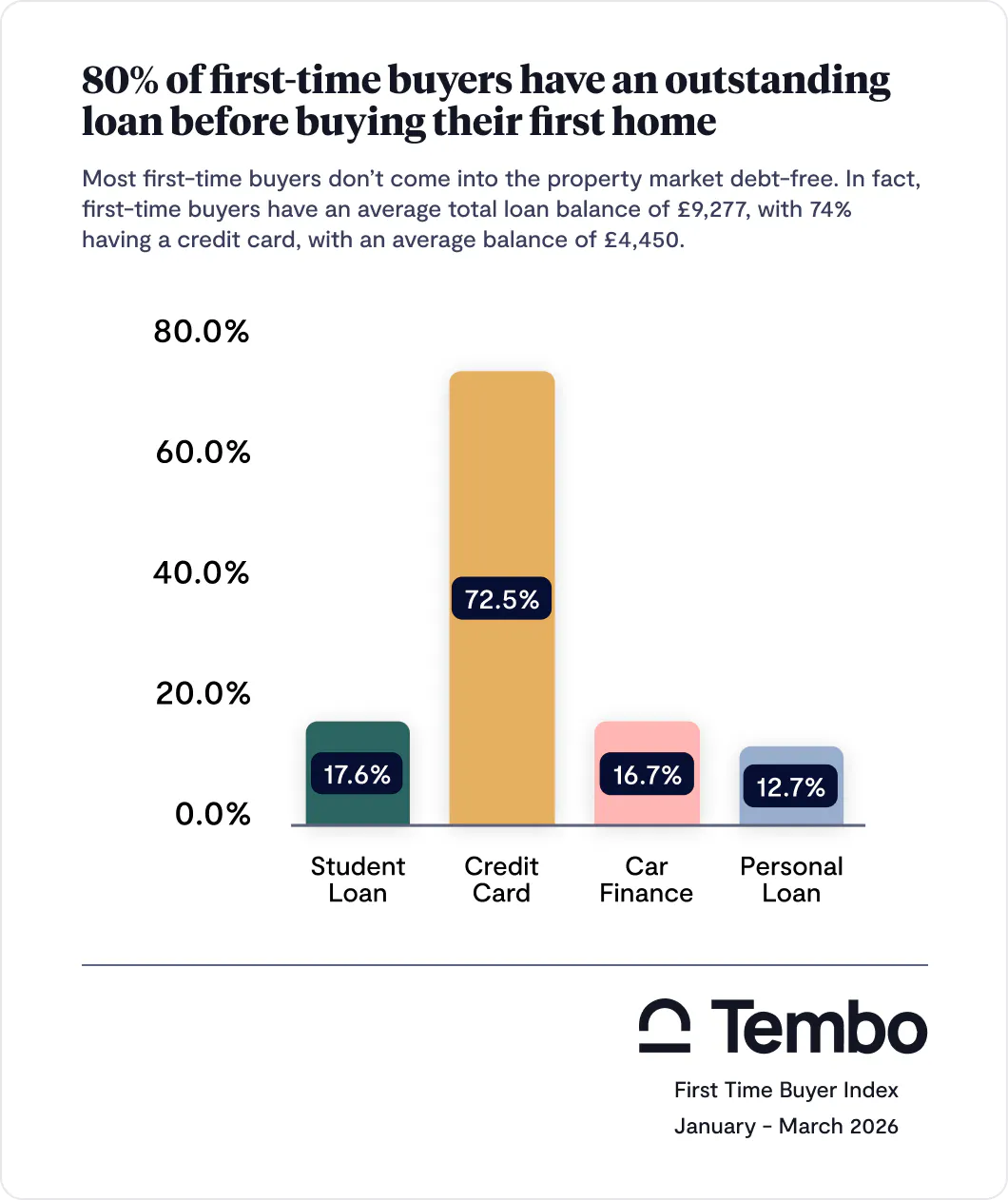

Majority of first-time buyers have strong credit ratings, despite 80% having outstanding loans

A poor credit score can be a significant barrier to entry for many aspiring home buyers. FCA data on mortgage sales shows that less than 1% of mortgages are made to people with impaired credit history.

But, in the first quarter of 2026, first-time buyers fared well, with the average credit score for first-time buyers being 670 out of 1,000 - which is deemed to be a “Good” credit score. Whilst the majority of first-time buyers had strong credit history over 530, and only 1 in 10 had a “Fair” or “Poor” credit score.

Most first-time buyers don’t come into the property market debt-free. Our analysis showed that 80% of first-time buyers had some form of loan outstanding prior to buying their home, with an average total loan balance of £9,277 - 74% of first-time buyers had a credit card, with an average balance of £4,450. Student loans were the next most common form of debt, with 18% of first-time buyers having on average £13,000 remaining.

You might like: What is a credit score and how does it impact getting a mortgage?

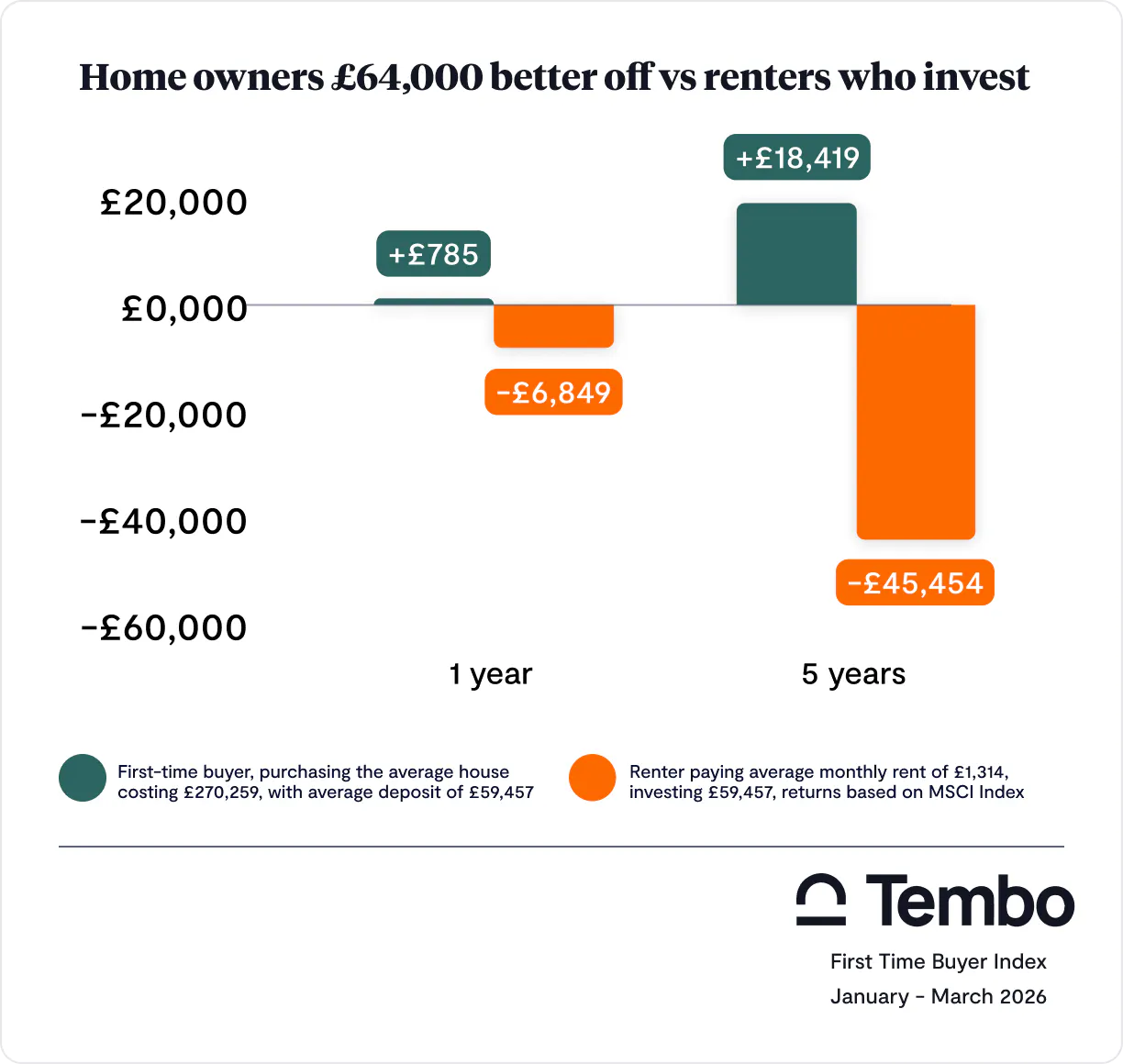

Home buyers are £64,000 better off after five years compared to those who rent and invest

“Is now a good time to buy” is a question many first-time buyers will - quite rightly - ask themselves before making the largest purchase of their lives. With so much uncertainty in the market, trying to time a first-time home purchase at exactly the right time can be very challenging.

Historical data shows consistently that 'time in the market', rather than 'timing the market', that is the key factor.

And our analysis backs this up.

When assessing whether it is better financially to buy, or to rent and invest over a 1-year and 5-year period, we found that home buyers are £7,600 better off after 1 year and £64,000 better off after five years compared to those renting.

However, this is not the same across the country, with local property price movements creating significant differences between areas.

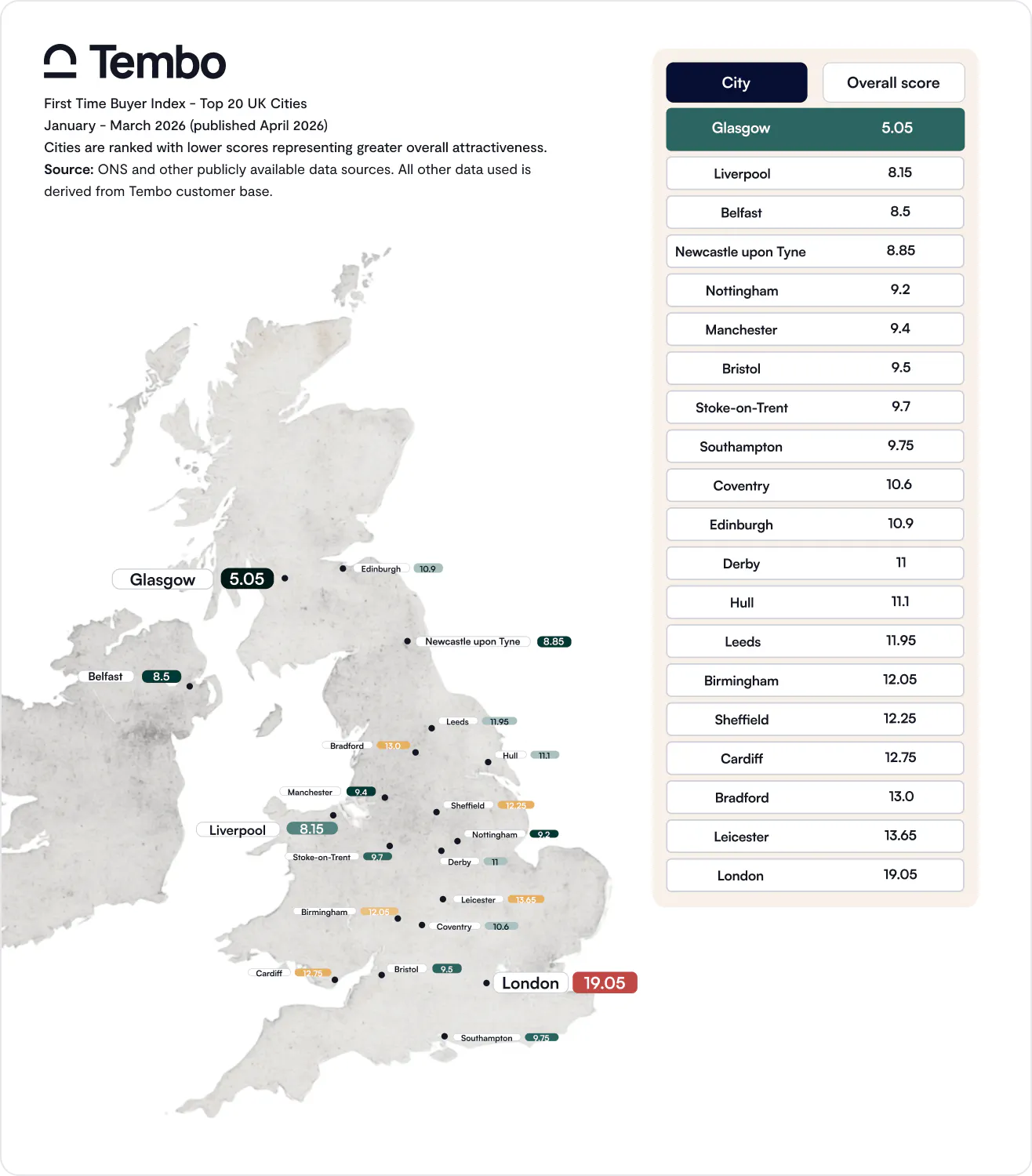

Where’s the best place to buy?

As part of the Tembo First Time Buyer Index, we've rated the 20 biggest cities in the UK and ranked them based on a mix of affordability and lifestyle factors to give them an overall score of their attractiveness to first-time buyers. Cities with lower scores represent greater overall attractiveness.

Want to see what you could afford in your city?

Discover your true buying budget with Tembo in minutes.

Glasgow leads on affordability and house price growth

If you’re looking for that sweet spot between affordability and long-term payoff, Glasgow comes out on top with an overall score of 5.1.

Buyers in Glasgow are borrowing way less compared to the rest of the UK, which is a big deal when you’re trying to stay within comfortable limits. But it’s not just about getting on the ladder; it’s also about what happens after. Glasgow has also seen the highest financial return for first-time buyers over the past five years as house prices have jumped 33%, which is double the UK growth rate average of 16.7%.

In real terms, that means a first-time buyer who bought in Glasgow five years ago would be £122,872 better off compared to renting and investing instead.

However, renting isn’t exactly cheap while you’re saving. People are spending about 37% of their income on rent, and the city is ranked 15th out of 20 for rent affordability, so it’s not the easiest place to build a deposit.

Still, once you’re in, it really starts to pay off. From a lifestyle perspective, Glasgow scores in the top 10 across the key Tembo indicators, which include factors like the number of pubs per square mile and the amount of green space per person.

London remains structurally unaffordable

London stands out as a clear outlier, where would-be home buyers are hampered by extreme financial pressures not found elsewhere. Rent consumes over half of income (51%), while loan-to-income ratios reach 8.3 - nearly double typical lending thresholds.

This restricts both the ability to save and to borrow, placing home ownership out of reach for many first-time buyers without external support. Despite this, London continues to score highly on lifestyle metrics, with strong performance on the number of amenities.

The result is a market where first-time buyers are trading affordability for access to the vibrant, well-connected capital.

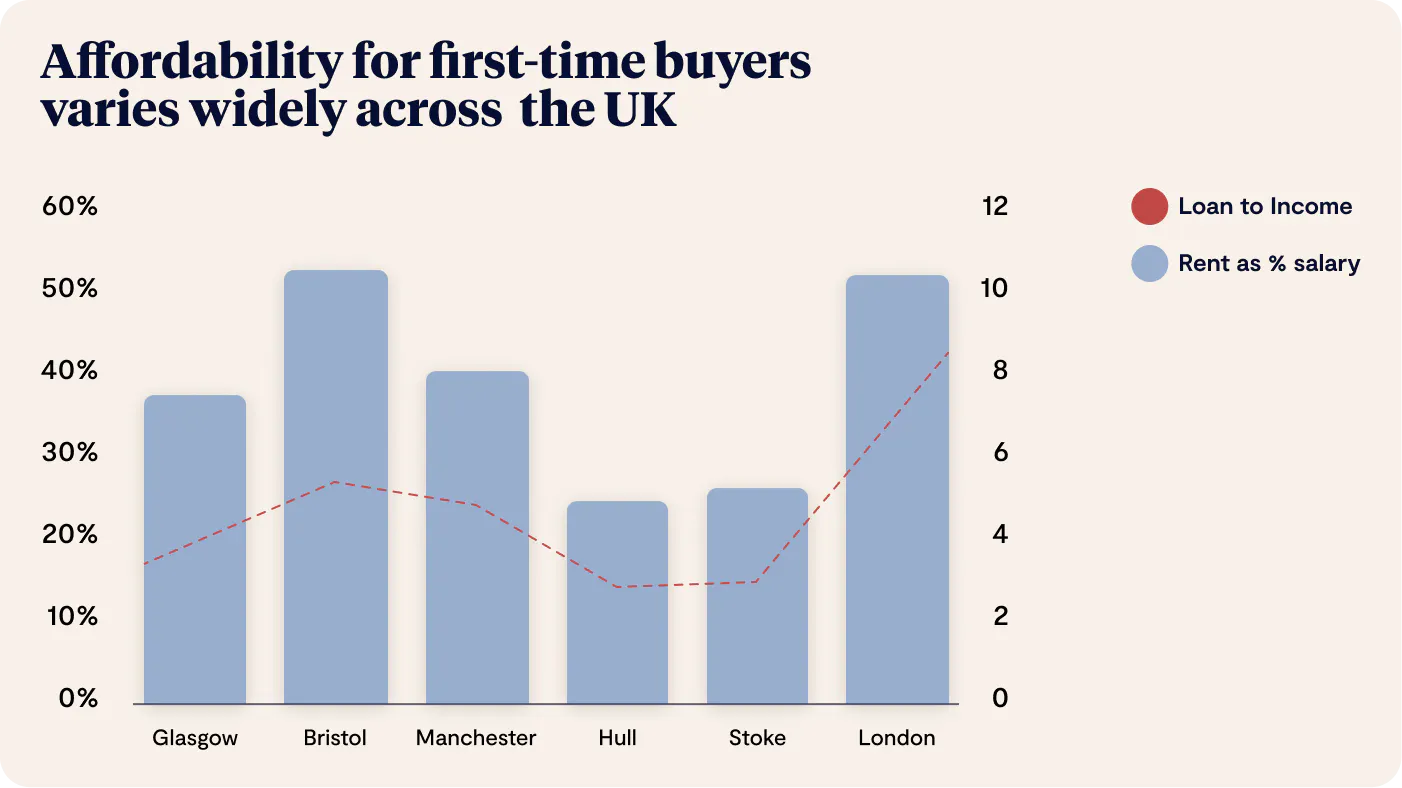

Affordability varies widely across the rest of the UK

At the most accessible end, cities such as Hull, Stoke, Derby and Bradford combine low rent-to-income ratios (22–25%) with modest loan-to-income multiples (2.6–3.5), reducing both the savings and borrowing barriers to homeownership. However, these cities tend to score lower on lifestyle measures, including amenities density.

At the other end, cities such as Bristol, Manchester and Edinburgh exhibit higher levels of financial pressure - with rent typically exceeding 39% of income and loan-to-income ratios above 4.4 - but continue to rank strongly overall due to higher house price growth and stronger performance on lifestyle indicators.

Tembo First Time Buyer Index - Top 20 UK Cities

| City | Rent as % of income | Loan to Income | Buy 5 years ago vs renting |

|---|---|---|---|

Glasgow | 36.92% | 3.14 | 122,872 |

Bristol | 52.07% | 5.62 | 112,495 |

Manchester | 39.04% | 4.49 | 100,374 |

Belfast | 36.48% | 3.74 | 96,897 |

Newcastle upon Tyne | 38.64% | 3.81 | 91,389 |

Edinburgh | 39.56% | 4.47 | 90,410 |

Southampton | 36.68% | 4.01 | 71,117 |

Nottingham | 34.50% | 3.99 | 69,811 |

Leeds | 35.07% | 4.35 | 68,597 |

Cardiff | 36.18% | 4.71 | 67,930 |

Liverpool | 27.81% | 3.42 | 67,515 |

Birmingham | 32.96% | 4.12 | 61,175 |

Coventry | 28.67% | 3.73 | 53,772 |

Sheffield | 29.41% | 4.03 | 52,896 |

Leicester | 34.75% | 4.74 | 52,487 |

Stoke-on-Trent | 23.21% | 2.95 | 46,800 |

Derby | 24.50% | 3.47 | 44,349 |

Bradford | 24.55% | 3.64 | 43,684 |

Hull | 22.51% | 2.66 | 40,972 |

London | 51.36% | 8.31 | 4,307 |

Struggling to get on the ladder?

Discover smarter ways you could increase what you can borrow by completing your details online with Tembo.

About the Tembo First Time Buyer Index

The Tembo First Time Buyer Index tracks affordability across the housing market for first-time home buyers, using sold prices, mortgage valuations and data for recently agreed sales. The methodology

The Tembo data used in this report is derived from mortgage details submitted by 8,000 prospective and actual first-time buyers, 1,000 Lifetime ISA savers and credit data from 100 first-time buyers.

Calculation of First-Time Buyer Attractiveness Score

The First-Time Buyer Attractiveness Score is a weighted composite score out of 1000, combining metrics such as loan-to-income ratios, interest rates, average disposable

income after mortgage repayments, loan-to-value ratios, time to sell properties, credit profiles, and five-year buy vs rent outcomes. Metrics are grouped into five categories -

affordability, deposit, time to buy, credit and financial outcomes - and aggregated

using predefined weightings.