How much tax do you pay on rental income?

Whether you are an accidental landlord or a professional Buy to Let investor, paying tax on rental income is part and parcel of the job. But how much tax do you pay on rental income? And what can you offset and expense? This guide explains how much tax you pay on rental income and how you could reduce your rental income tax bill while staying on the right side of HMRC.

In this guide

- What counts as rental income?

- Is rental income taxable?

- What expenses can you deduct from rental income?

- How is tax on rental income calculated?

- How much rental income is tax-free in the UK?

- Can I deduct mortgage interest from rental income?

- How can I avoid paying tax on rental income?

- Rental income tax FAQs

Tax treatment depends on individual circumstances and may be subject to change in the future. This article is for informational purposes and does not constitute financial advice. Please consult a financial advisor or tax advisor before making any decisions which could affect your financial situation.

Key takeaways

- Tax rates: Rental income is taxed at your marginal rate (20%, 40%, or 45%) based on your total annual income.

- Property allowance: The first £1,000 of your rental income is tax-free each year.

- Mortgage interest: You cannot deduct mortgage interest as an expense, but you receive a 20% tax credit on interest payments.

- Allowable expenses: You can reduce your tax bill by deducting costs like repairs, insurance, and letting agent fees.

- Tax efficiency: Splitting rental income with a partner in a lower tax bracket can significantly reduce your overall liability.

What counts as rental income?

Rental income is made up of the money your tenants pay in rent, along with anything they pay you towards utility bills, repairs, cleaning fees for communal areas, and non-refundable deposits. If you receive any rent in advance … this still counts as rental income in the tax year you receive it. If you keep a portion of their tenancy deposit when they move out of the property, this is classed as rental income too, even if you’re spending this money on repairs and maintenance.

For example, your tenants pay you £12,000 a year in rent. At the end of their tenancy, you keep £100 from their deposit to cover the cost of repairs, and you keep an additional £50 for cleaning fees. This means your total rental income over the course of that year is £12,150.

Non-cash payments also count, for example, if a tenant paints a hallway in return for £300 of rent, that £300 is taxable rental income.

Learn more: Can I change my mortgage to Buy to Let?

Is rental income taxable?

Yes, you do pay tax on rental income. The good news is that many of these costs can be deducted as expenses, allowing you to reduce your taxable income and keep more money in your pocket.

If you have a rental income, you must:

- Register for Self Assessment by 5th October after the end of the tax year.

- File the online Self Assessment tax return by 31st January.

- Pay any tax owed by 31st January (and make any payments on account if needed).

Looking to remortgage an existing Buy to Let?

See what mortgage options you are eligible for from over 100 lenders by completing your details online with Tembo - the UK’s Best Mortgage Broker four years running.

What expenses can you deduct from rental income?

When renting out a property, it’s important to keep track of your expenses. Here are some of the most common allowable expenses for rental income:

- Travel costs (to and from your rental property)

- Advertising and marketing costs

- Phone bills (in relation to your rental property)

- Cost of safety certificates

- Advisory fees, e.g. legal and accountancy

- Subscription to property investment-related magazines, products and services

If you own a residential rental property, you can also expense the following:

- Letting agents’ fees

- Legal fees for leases of a year or less, or for renewing a lease for less than 50 years

- Accountants’ fees

- Buildings and contents insurance

- Maintenance and repairs to the property (but not improvements)

- Utility bills, like gas, water and electricity

- Rent, ground rent, service charges

- Council Tax

- Services you pay for, like cleaning or gardening

- Other direct costs of letting the property, like phone calls, stationery and advertising

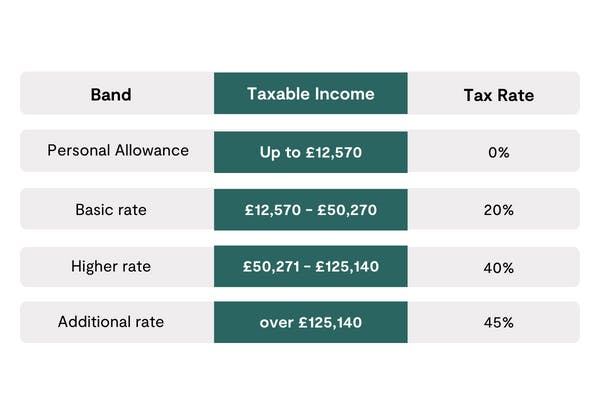

How is tax on rental income calculated?

The amount of tax you’ll pay on rental income depends on your tax bracket and the amount you earn. Rental profits will be taxed at the same rate as any income from your business and employment.

However, in some circumstances, your rental income could push you into a higher tax bracket. For example, let’s imagine you earn £40,000 from full-time employment and £12,000 in rental income during the same tax year, with a total income of £52,000, you’ll find yourself in the higher rate tax bracket of 40%.

Thankfully, you won’t be charged 40% on your total income. The first £12,570 of your total income will continue to be tax-free. Anything you earn between £12,571 and £50,270 will be taxed at 20%, and only the amount above £50,271 will be taxed at 40%.

You can use the Take Home Pay Calculator to see what you could bring home each month after tax.

It may be possible to reduce your taxable income by claiming expenses. If you earn £52,000 from employment and rental income but you claim £3,000 in expenses, your taxable income will be £49,000, bringing you back into the basic rate tax band.

Learn more: How to get a Buy to Let mortgage

How much rental income is tax-free in the UK?

The first £1,000 of rental income is tax-free. This is known as your ‘property allowance’. Landlords who rent out a furnished room in their own home may be able to use the Rent a Room Scheme instead, which allows up to £7,500 a year in rental income to be tax-free (or £3,750 each if the income is shared). After this, you must file a Self Assessment tax return if your rental income is either:

- £2,500 to £9,999 after allowable expenses

- £10,000 or more before allowable expenses

If your rental income is between £1,000 and £2,500 a year, you should contact HMRC for more information. It may be possible to pay the tax via PAYE (if employed), saving you the hassle of having to complete a Self Assessment tax return.

Can I deduct mortgage interest from rental income?

You can no longer deduct mortgage interest from rental income, following changes to the way that landlords are taxed. Under the previous system, landlords could reduce their tax bill by claiming mortgage interest as an expense - this all changed in April 2020. The new system offers landlords a tax credit based on 20% of their mortgage interest.

Under the new system, higher-rate taxpayers who previously deducted mortgage interest at 40% now receive a 20% tax credit instead, which may result in a higher tax bill for some landlords.

Learn more: Is Buy to Let worth it in 2026?

See how much you could get for a Buy to Let

Fill in your details with Tembo and see your mortgage options from over 20,000 mortgages in less than 10 minutes.

How can I avoid paying tax on rental income?

While rental income is taxable, there are several legitimate ways to reduce your tax liability through allowable expenses and strategic planning. A couple of options are listed below, but it's always best for you to speak to a tax specialist to get expert advice.

1. Claim costs for void periods

If a Buy to Let property is empty for any period of time, you can expense running costs such as energy bills and council tax.

2. Carry forward your losses

If you’ve made significant rental losses in previous tax years but your Buy to Let property is now profitable, you may be able to lower your tax bill by carrying your previous losses forward.

3. Don’t forget your home office

It’s possible to claim expenses for the cost of running your home office, even if you only have one rental property. Home office costs can include electricity, broadband and home insurance, for example.

4. Buy your rental property with someone else

You may be able to reduce your tax bill by purchasing a Buy to Let property with a friend, family member or business partner and splitting the rental income between you.

This can be particularly effective for higher-rate and additional-rate taxpayers who’d like to help a child or grandchild invest in property.

For example, if you earn £60,000 a year and you’d like to purchase a Buy to Let property.

If you buy the property alone, your rental income will be taxed at 40% (since you’re already a higher-rate taxpayer).

If you buy the property alongside their daughter, who earns £25,000 a year, her share of the rental income will be taxed at 20%. By reducing the amount of tax payable, your Buy to Let could be more profitable.

You can decide how to divide the rental income. It doesn’t need to be split 50/50, and it doesn't need to reflect the amount each party has invested in the property. Dividing the rental income in favour of the lower taxpayer tends to be more tax-efficient, as long as this income doesn’t push them into a higher tax bracket.

If you would like to help a loved one get on the property ladder, Tembo can help them find the right guarantor mortgages and first-time buyer schemes for them.

If you buy a rental property with your spouse or civil partner, you’ll usually have what’s known as a ‘joint tenancy’ or joint mortgage and the rental profits will automatically be split 50:50. If this isn’t a tax-efficient way of dividing your profits, contact HMRC to see if it’s possible to change the way your rental income is divided.

5. Buy through a limited company

You may choose to buy and hold rental property through a limited company. In many cases, mortgage interest and other finance costs can be treated as a business expense in a company, which can make this route more tax-efficient for certain borrowers, although company ownership can also involve different mortgage products, fees, and tax considerations.

See what you could be offered

Whether you’re an existing landlord or you want to buy your first Buy to Let property, you can see your mortgage options from +100 online for free with Tembo, including live rates and indicative monthly repayments.

Rental income tax FAQs

Can you offset mortgage payments against rental income?

No, you cannot offset mortgage payments or interest as a direct expense. Instead, you receive a 20% tax credit. For example:

- Mortgage Interest Paid: £10,000

- Tax Credit Calculation: 20% of £10,000

- Total Tax Relief: £2,000

Does rental income count as earned income?

No, rental income doesn't count as earned income, unless the landlord is renting out a furnished holiday home. If you’re the owner of a Buy to Let property, the income your property generates is classed as ‘unearned income’. While earned income is money you make from working, such as a salary, wages or tips, unearned income is money you receive without performing work, such as interest, dividends or rental income.

Do you pay national insurance on rental income?

You won’t usually need to pay National Insurance contributions on rental income, since it's treated as ‘unearned’ income. However, Class 2 National Insurance may apply if letting property is treated as running a business.

Do you need to file a Self Assessment tax return for rental income?

You typically need to file a Self Assessment tax return if your rental income is £10,000 or more before allowable expenses, or between £2,500 and £9,999 after allowable expenses.

What happens if rental income isn’t declared to HMRC?

If rental income isn’t declared, HMRC may charge interest and penalties on unpaid tax. If you have undeclared rental income, you may be able to disclose it through HMRC’s Let Property Campaign.

Can rental income push a landlord into a higher tax bracket?

Yes, rental income is added to other income when working out which tax band applies, so it can push you into a higher band. Claiming allowable expenses can reduce taxable rental profit and may help keep total taxable income within a lower band.

How is rental income taxed on a jointly owned property?

For spouses and civil partners, rental profits are usually split 50:50 by default. If ownership shares are different and landlords want the tax split to reflect those shares, it may be possible to declare the actual beneficial interests to HMRC (for example, using Form 17).

When is the deadline to register for Self Assessment for rental income?

You generally need to register for Self Assessment by 5th October after the end of the tax year in which the rental income was received.