How to reduce inheritance tax

Inheritance tax is part of a system that aims to redistribute wealth and finance public spending along with other taxes such as Income Tax, Corporation Tax and VAT. Inheritance tax is paid on a person's estate when they die.

With significant increases in the value of property and investments in recent years the amount of inheritance tax being paid has increased. Three quarters of property wealth in the UK is in the hands of over 55s. This in turn means that many younger people are set to inherit substantial sums over the next few decades. So it’s understandable that many families want to reduce the amount that will go to HMRC and increase what their loved ones will receive in inheritance.

With the help of some careful tax planning, financial advice, and generous gift giving, you can make the most of your money and protect those you care about. Keep reading to find out more.

What is inheritance tax?

Inheritance tax is a tax on the estate of someone who’s died, including their property, money and possessions. You only pay inheritance tax if the value of the estate is over £325,000, in which case you’ll pay 40% for anything over the threshold.

Who pays inheritance tax?

The good news is that most people don’t pay any inheritance tax. You'll only pay inheritance tax if the value of your estate is above the £325,000 threshold, or you leave everything above the £325,000 threshold to your spouse, civil partner, a charity or a community amateur sports club.

If you give your home to your children or grandchildren, your threshold can increase to £500,000. If you’re married or in a civil partnership and your total estate is worth less than the threshold, the difference between your estate’s value and the threshold can be added to your partner’s threshold when you pass away.

How much is inheritance tax?

The standard Inheritance Tax rate is 40%, but it’s only charged on the part of your estate that’s above the £325,000 threshold.

So, if your estate is worth £500,000 and your tax-free threshold is £325,000, your estate will be taxed at 40% on the remaining £175,000.

Does a spouse pay inheritance tax?

Marriage and civil partnerships have multiple financial benefits. One of them is the ability to pass money and assets between you and your spouse/civil partner tax-free. This means that if a husband or wife dies and leaves their whole estate to their widow, no inheritance tax will be payable.

When do you pay inheritance tax?

Inheritance tax must be paid by the end of the sixth month after the person’s death. HMRC will start charging interest if it’s not been paid in time. However, it is sometimes possible to split the tax bill into instalments and pay them over a period of up to 10 years, but interest will be added onto the outstanding amount.

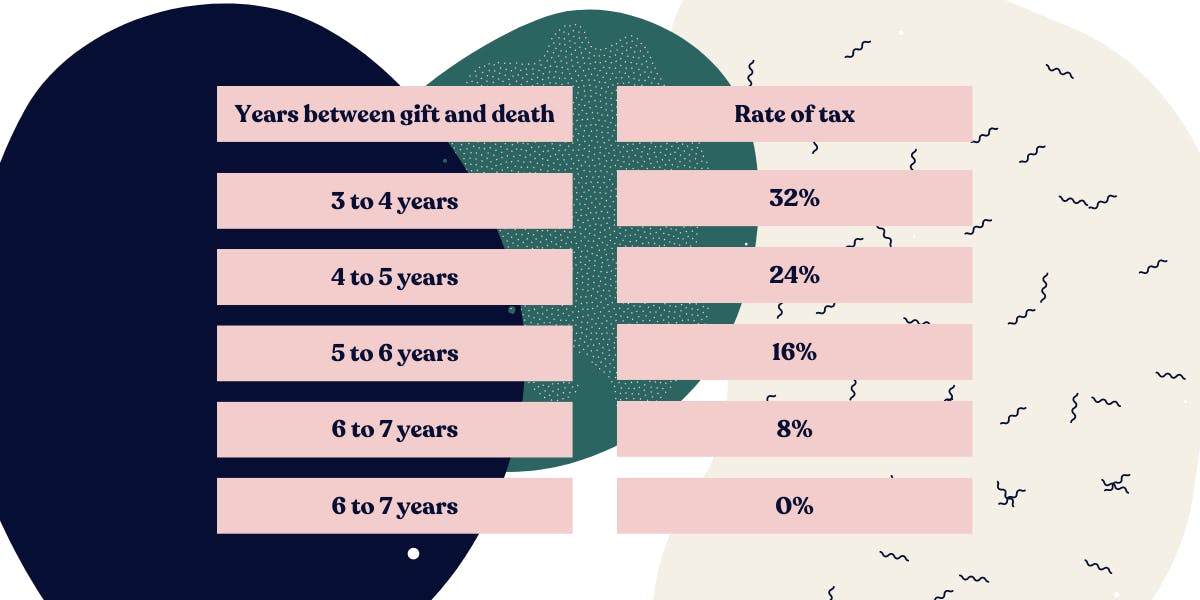

What is the 7 year rule on inheritance tax?

If you give assets away during your lifetime and survive for at least 7 years afterwards, then all gifts are free from inheritance tax. These gifts are known as potentially exempt transfers. If you die within 7 years of giving assets away, you’ll pay inheritance tax - but the exact rate can vary. Gifts given in the 3 years before your death are taxed at 40%, while gifts given 3 to 7 years before your death are taxed on a sliding scale known as ‘taper relief’.

Taper relief only applies if the total value of gifts made in the 7 years before you die exceeds the £325,000 tax-free threshold.

How do people avoid inheritance tax?

Since only 4% of people pay inheritance tax, you might assume it’s a tax paid only by the rich, but this isn’t necessarily the case. There are so many inheritance tax rules, exemptions and loopholes, that wealthy people often hire financial planners and tax experts to help them make their estate more tax-efficient. Their properties, savings and investments will be carefully curated and managed with inheritance tax in mind.

Useful To Know

There’s nothing illegal about hiring an estate planning expert to help you get your affairs in order. And even if you’re not rich, there are plenty of things you can do to reduce your inheritance tax bill.

How to reduce inheritance tax

If you’re wondering how to reduce inheritance tax, here are 6 ways to reduce your inheritance tax bill:

1. Make a will

Making a will is one of the easiest ways to manage your estate and make sure your money goes to the people you care about the most. Without a will, your assets could be distributed by the government.

A will can also help you reduce your inheritance tax bill. For example, you might use your will to set up a trust. This is a legal arrangement where you give cash, property or investments to someone else to take care of them on behalf of a beneficiary. When you pass away, any assets held within the trust are likely to be exempt from inheritance tax.

2. Spend your money

Research suggests people spend less money when they get older, but if you’re financially comfortable and have enough to last, your later years are the perfect time to treat yourself and your family. There are no prizes for being the richest person in the graveyard, after all.

Pick up the bill in the restaurant. Pay for driving lessons. Book a spa break. The more you spend, the less your loved ones’ inheritance will be taxed on when you pass away.

3. Help your children buy a home

Young people today are finding it harder than ever to buy their first home, especially with house prices rising faster than wages. Our research suggests a quarter of young adults will inherit more from the Bank of Mum and Dad than they’d earn over 40 years of work. While this may be good news for those standing to inherit large sums, most will have to wait until their 40s, 50s or older to receive such a large windfall. Until then, buying a house will remain an impossibility for most!

This is where Tembo comes in.

If you’ve managed to amass a large amount of equity in your home and you’d like to help your children or grandchildren get on the ladder, talk to Tembo. We’re big believers of the benefits of an early inheritance.

For example, if your child is struggling to save a big enough deposit, a Deposit Boost could be the answer. You’ll be able to unlock money from your home through a small second mortgage. The proceeds would be gifted to your child to boost their own mortgage deposit, or mean they don’t need to save up a house fund themselves.

If you give the funds to your child as a gift (rather than offering them an informal loan) and live for at least 7 years, the money won’t be taxed when you pass away. For £100,000 that you gift, this could potentially save your family £40,000 Inheritance tax on your estate when you die.

Interested in a Deposit Boost?

To see if you're eligible for a Deposit Boost, simply create a free Tembo plan today. It takes 10 minutes to complete, and there's no credit check involved. At the end, you and your child will get a personalised recommendation of all the buying schemes they're eligible for, and what they could afford.

4. Pay for your funeral now

Save your loved ones time, stress and money by planning your funeral yourself and paying for it before you kick the bucket. The money you spend on your funeral won’t count towards your estate and so you won’t be taxed on it.

5. Take out life insurance

Some people choose to take out a life insurance policy to cover their inheritance tax bill. By placing the policy in a trust, you can ensure it’s paid outside of your estate.

6. Give generously

There are several inheritance tax rules that encourage you to give money away to reduce your inheritance tax liability.

These include:

- Marriage. Married couples can transfer assets between them tax-free.

- Annual exemption. Each tax year you can give a gift of up to £3,000 to anyone you like. If you didn’t make use of this exemption in the previous year, you can give twice as much.

- Small gifts. You can gift anyone up to £250 each tax year, as long as you’ve not given that same person any other gifts during the same year.

- Wedding gifts. You can gift your children up to £5,000 and your grandchildren and great-grandchildren up to £2,500 for a wedding. You can give other relatives or friends up to £1,000 when they get married.

- Charities and political parties. You can make donations to charities or political parties, inheritance tax-free, both in your lifetime and in your will. If you leave at least 10% of your new estate to charity in your will, the rate of inheritance tax reduces to 36%!

- Extra income. If, after paying income tax, you have extra income that you don’t need, you can use it to make regular gifts. You may need to keep a record of these using a form called HMRC IHT403, though.

If you’re thinking of helping your child get on the ladder, talk to Tembo. Our team of specialist mortgage brokers can walk you through what options are available for you and your family. Although we don’t advise on tax ourselves, we do work with leading financial advisors who can advise you on how you can optimise your estate management to reduce your inheritance tax liability, depending on what your needs are. Get in touch to get started.

We've helped thousands of buyers with family lending

If you want to help your child get a place of their own, talk to Tembo. Our award-winning team are experts when it comes to family assisted mortgages. We can help you and your family find the best guarantor mortgage or specialist buying scheme for you. Simply create a free Tembo plan to get started